Weekly Market Pulse - Week ending November 24, 2023

Market developments

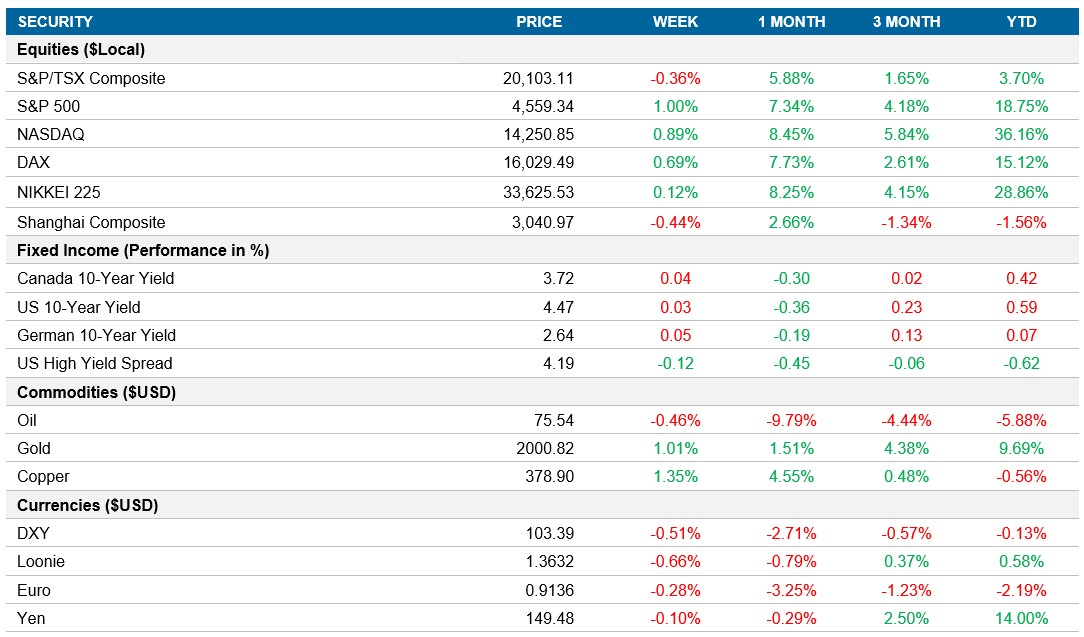

Equities: Global equity market saw mixed reactions in a week marked by a 1% rise in the S&P 500. Nvidia Corp's stock faced a downturn following news of a delayed AI chip launch, highlighting the market's sensitivity to tech sector movements. Investor sentiment was also influenced by contrasting views from financial analysts, with some predicting cautious near-term outlooks due to inflation and growth concerns, while others anticipated bullish trends, forecasting significant gains for the S&P 500 by the end of 2024. This mixed sentiment underscored the ongoing market uncertainty and divergent expectations regarding future economic and monetary policies.

Fixed income: During the week, the U.S. Treasury market experienced notable shifts primarily driven by economic data. Yields were impacted by jobless claims and consumer sentiment indicators, which suggested persistent inflationary pressures. This led to a bear flattening of the yield curve, with shorter and mid-term yields rising more sharply than longer-term yields.

Commodities: In the commodities market, the focus was on the oil sector, influenced by OPEC+ dynamics. Brent crude futures fluctuated, settling around $75 a barrel towards the end of the week. The Organization of Petroleum Exporting Countries and its partners are trying to resolve a disagreement over output quotas, specifically regarding targets set for Angola and Nigeria for 2024.

Performance (price return)

As of November 24, 2023

Macro developments

Canada – CPI Decrease and Retail Sales Increase in Canada

Canada's Consumer Price Index (CPI) showed a continued disinflationary trend in October, with the headline CPI dropping to 3.1% year-over-year from September's 3.8%. This decrease was largely influenced by a significant decline in gasoline prices, leading to goods inflation falling to 1.6%. On the other hand, services inflation rose, primarily due to higher mortgage interest costs and persistent rent inflation amidst a housing shortage.

Concurrently, Canadian retail sales in September and preliminary data for October indicate a rebound after a weak third quarter. Despite a contraction in retail sales volumes over the third quarter, sales values increased by 0.8% month-over-month in October, suggesting a stronger rebound in volumes. This increase was driven by rising sales in gasoline and motor vehicles, while core retail sales experienced a slight dip.

U.S. – PMI Stagnation Amidst Subdued Demand and Employment Decline

November 2023 saw a notable change in the U.S. private sector, as reported in the PMI survey, with employment declining for the first time since June 2020 amid muted demand conditions. The Flash US PMI Composite Output Index remained steady at 50.7, indicating only marginal growth in business activity. While the services sector noted a slight increase, manufacturing output experienced a downturn. This period of weak demand led to workforce reductions, the first in over three years, as both manufacturers and service providers adjusted to the challenging economic environment. Additionally, input price inflation showed signs of easing, marking the slowest increase since October 2020.

International – Japan's Stagnation, Eurozone Downturn, UK Stabilization

In Japan, November's private sector activity showed signs of stagnation, with the Flash Composite Output Index holding steady at 50.0. While services business activity saw a modest increase to 51.7, manufacturing output significantly declined to 46.4, marking the most substantial drop in nine months. Demand conditions remained muted, with manufacturing experiencing a notable decline in new work, though services noted a slight uptick in business. Input price inflation in Japan eased to a 27-month low, but remained high due to rising costs of raw materials, labor, and ongoing exchange rate weaknesses.

In Europe, the Eurozone's economic downturn persisted into November, with the Flash Eurozone Composite PMI Output Index slightly increasing to 47.1. This marked the sixth consecutive month of decreasing business activity, with both service and manufacturing sectors experiencing contractions. The decline in new orders led companies to reduce staffing levels for the first time since early 2021. Input cost inflation reached a six-month high, predominantly driven by rising service sector wages, while manufacturing costs continued to decrease. Despite these challenges, business confidence in the Eurozone remained moderately optimistic.

The UK economy showed signs of stabilization in November, primarily due to renewed growth in the service sector. The Flash UK PMI Composite Output Index rose to 50.1, a four-month high, with services business activity slightly increasing to 50.5. However, manufacturing continued to decline. Subdued underlying demand conditions persisted, as indicated by a continuous decrease in total new order intakes. Inflation concerns remained, with both input costs and prices charged accelerating, particularly in the service sector. Business activity expectations for the year ahead improved slightly, driven by rising confidence in the service sector.

Quick look ahead

As of November 24, 2023