Weekly Market Pulse - Week ending February 3, 2023

Market developments

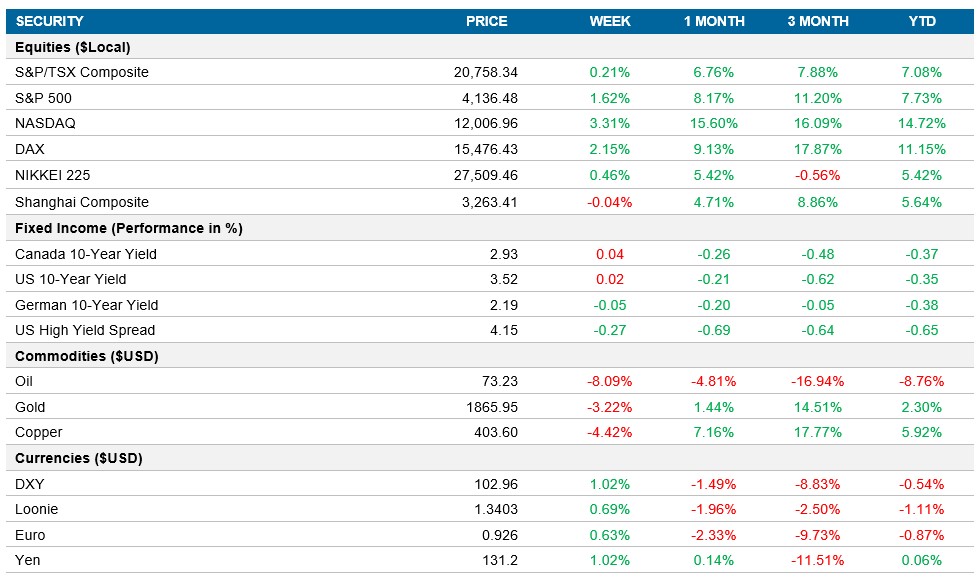

Equities: The U.S. market ended the positive week with a negative day on Friday as the combination of Amazon, Alphabet and Apple earnings drove the market lower. The S&P 500 gained over 1.6% and the Nasdaq rose +3.3% for the week as investors believe the economy is on firm footing, the Federal Reserve signalled they are near the end of this tightening cycle and Meta gained ~20% after a strong quarter. Warnings from large tech companies, along with a surprisingly strong jobs report drove the S&P 500 down -1% on Friday and the Nasdaq -1.5%. Europe ended the week +1.2% as lower than expected inflation and the signal that the end of the tightening cycle is in sight drove equities higher.

Fixed income: The fixed income market reacted more rationally after the FOMC announcement, as shorter duration treasuries spiked now that additional rate increases are expected. The 2yr U.S. Treasury yield climbed by 10bps to 4.29% for the week after a 19bps jump or Friday, while the 10yr U.S. Treasury yield remained relatively unchanged at 3.52% for the week after a 13bps increase to end the week. The U.S. market is now pricing in a higher peak rate (~5%) and a higher rate to end 2023 compared to a week ago.

Commodities: Oil dropped by 8% this week, closing at $73.24 as longer-term headwinds drove the price down. The record low unemployment in U.S was overwhelmed by the concerns of stockpiling inventory in the U.S. and weaker than expected demand from China.

Performance (price return)

As of February 3, 2023

Macro developments

Canada – Canadian economy grew by 0.1% in November, Manufacturing PMI climbed to 51

The Canadian economy expanded 0.1% in November, adding to the 0.1% we saw in October. Estimates indicate that the economy grew by 0.4% QoQ in Q4 of 2022, a deceleration from the 0.7% growth in Q3. Growth was seen in 70% of the industrial sectors as service producing industries outweighed a contraction in goods.

S&P Global Canada Manufacturing PMI rose to 51 in January, up from 49.2 in December. This marked the first month of a reading above 50 in the last five months as we saw gains in both production and new orders. Input prices increased at the slowest pace in the last 2.5 years, while companies hired additional workers at the fastest rate since July 2022.

U.S. – The Fed raised interest rates by 25bps, ISM Manufacturing slows as Services jump, Non-Farm Payrolls adds 517K Jobs, average hourly earnings slow to 4.4% YoY and unemployment rate comes in at 3.4%

As expected, the Fed raised the target range for the funds by 25bps to 4.5% - 4.75%, leaving borrowing costs at the highest level since 2007. The statement added that ongoing increases will be appropriate to bring inflation back to the 2% target. Powell commented that we are in the early stages of disinflation and that there is more work to be done to continue to battle high inflation.

ISM Manufacturing fell to 47.4 in January, below expectations of 48 and the lowest level since May 2020. January marked the third consecutive contraction in activity as outputs slowed to match slowing demand. The ISM services PMI increased unexpectedly to 55.2 in January, well above the 49.2 reading in December and beating market forecasts of 50.4.

The U.S. created 517K jobs in January, well above the market forecast of 185K. The growth was widespread, led by leisure and hospitality, professional/business services, and health care. The January data continues to show a tight labour market, even as we see big tech companies lay off workers to manage costs as they anticipate an economic slowdown. The unemployment rate fell to 3.4%, below expectations of 3.6% The average hourly earnings increased 4.4% YoY in January, 10bps ahead of market expectations, but below the previous month’s reading of 4.6%.

International – Eurozone GDP expanded by 0.1%, CPI slowed to 8.5% and both the ECB and Bank of England raise interest rates by 50bps, China PMI increase sharply and Japan retail sales beat expectations

Eurozone GDP grew by 0.1% in Q4 of 2022, decelerating from a 0.3% last quarter but ahead of the market forecast of -0.1%. However, it still marks the weakest pace of expansion since Q1 of 2021 as demand was impacted by high inflation and high interest rates. We saw expansion in Spain and France, while Germany and Italy contracted in Q4.

CPI in the Eurozone slowed to 8.5% in January, falling from the 9.2% in December and below market expectations of 9%. Core inflation remained at 5.2%, signaling that price pressures outside of energy, food, tobacco, and alcohol remain elevated, with energy prices slowing to 17.2% vs 25.5% is driving the headline number down to 8.5%

Eurozone unemployment rate came in at 6.6% in December, ahead of November’s 6.5% and above market expectations for the rate to remain at 6.5%. The ECB also raised interest rates by 50bps to 3% in the meeting this week, with a commitment to raise it by another 50bps in March. They also stated that they would keep raising rates at a steady pace and hold them higher to return inflation to the target of 2%. Bank of England also raised rates by 50bps to 4% during the February meeting, pushing borrowing costs to the highest levels since the end of 2008.

China Manufacturing PMI increased to market expectations of 50.1, up meaningfully from the 47.0 in the previous month and the first expansion since last September. Non-Manufacturing PMI also increased meaningfully to 54.4 in January, up from 41.6 the month before and above market expectations of 52 as we see the impact of the government lifting the zero-Covid policy.

Japan retail sales came in at 3.8%, ahead of market expectations of 3.1% and a sharp increase from the 2.5% in November. The jobless rate in Japan remained unchanged in December at 2.5%, in line with market forecasts.

Quick look ahead

As of February 3, 2023