Weekly Market Pulse - Week ending May 26, 2023

Market developments

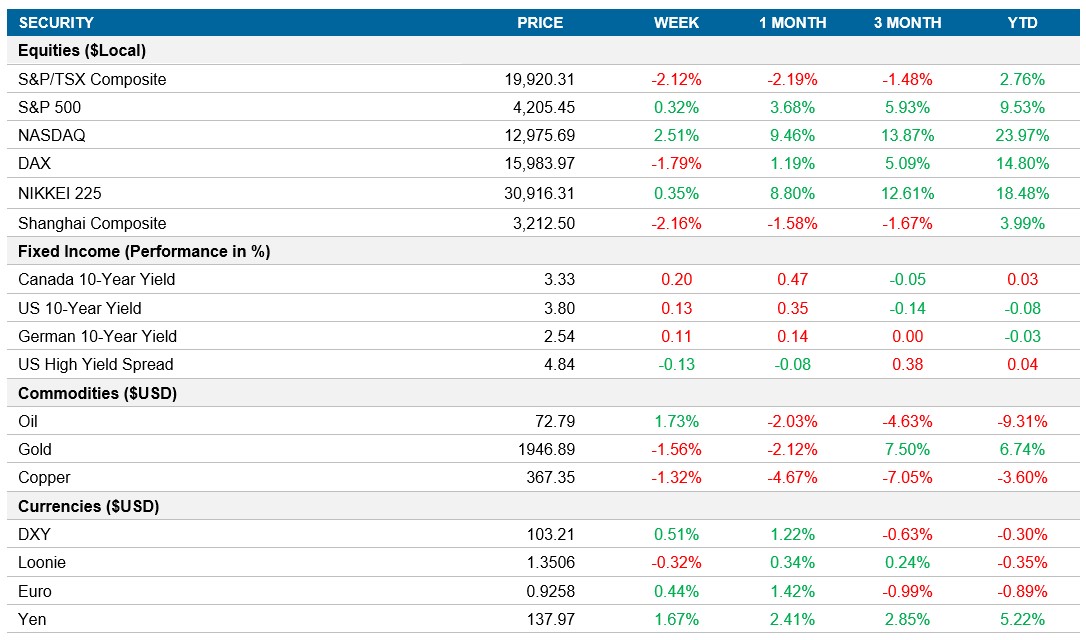

Equities: The stock market saw another week of gains driven by the enthusiasm surrounding artificial intelligence (AI) and growing confidence in the U.S reaching a deal on their debt limit. The S&P 500 climbed 0.3%, and the tech-heavy Nasdaq surged 2.5% following Nvidia Corp.’s earnings release caused a 32% price surge. Alongside the AI optimism, progress in US debt limit negotiations added to market positivity, as House Speaker Kevin McCarthy expressed belief in recent advancements. The S&P 500 closed above 4,200 for the first time since August 2022.

Fixed income Treasury bills expiring in early June yielded less than 6% on Friday as the likelihood of reaching a debt deal increased. Meanwhile, the two-year Treasury yield hovered around 4.56% as traders considered the impact of a debt deal on the Federal Reserve's interest rate trajectory. The consumer spending report revealed that the Fed still has work to do in achieving its inflation target. Analysts noted that a debt resolution before the Federal Open Market Committee (FOMC) meeting could reduce the need for Fed rate hikes, but failing to meet the debt ceiling deadline would have severe consequences and eliminate the possibility of a rate hike.

Commodities: Oil prices experienced a second consecutive week of gains as investors closely monitored progress in debt-ceiling talks to avoid a U.S. default. Meanwhile, supply dynamics remained in focus as conflicting statements from Saudi Arabia and Russia created uncertainty regarding potential production cuts by OPEC and its allies. The lackluster economic recovery in China, a top importer of oil, and the U.S. Federal Reserve's aggressive monetary tightening campaign have contributed to a nearly 10% decline in crude prices this year.

Performance (price return)

As of May 26, 2023

Macro developments

Canada – No Notable Releases

No notable releases this week

U.S. – U.S. PMI Expansion Gains Momentum in May, U.S. Economy Grows by 1.3% in Q1 2023, U.S. Personal Consumption Prices Rise in April

The S&P Global U.S. Composite PMI rose to 54.5 in May, indicating the fastest expansion in the country's private sector since April 2022. Service sector growth reached a 13-month high, supported by robust demand conditions. Manufacturing production saw only slight improvement, while total new orders increased for the third consecutive month. Employment levels surged at the quickest pace since July 2022. Input prices fell for manufacturers for the first time in three years, while service providers faced rising cost burdens. Output charge inflation remained elevated. Businesses are optimistic about the future, expecting increased demand and planning investments in new products and marketing.

The U.S. economy expanded by 1.3% in the first quarter of 2023, slightly surpassing initial estimates. Consumer spending showed resilience, growing at a faster-than-expected rate of 3.8%, despite persistent inflation. Non-residential fixed investment and public spending also saw upward revisions. However, residential fixed investment contracted further, and private inventory investment remained a drag on GDP, albeit less severe than previously estimated. Net external demand contributed positively, with exports outpacing imports. Nonetheless, Q1 2023 marks the slowest growth since Q2 2022.

In April, the United States witnessed a 0.4 percent month-over-month increase in the personal consumption expenditure (PCE) price index, following a 0.1 percent rise in March. Prices for goods rebounded, rising by 0.3 percent after a 0.2 percent decline in the previous month, while services inflation accelerated to 0.4 percent from 0.3 percent. Food prices experienced a slight decrease of less than 0.1 percent, compared to a 0.2 percent decline, and energy prices rose by 0.7 percent, recovering from a 3.7 percent decline. Excluding food and energy, the PCE price index rose by 0.4 percent, surpassing market expectations of 0.3 percent.

International – U.K. Consumer Price Inflation Eases to 8.7% in April but Remains High, Eurozone Composite PMI Drops to Three-Month Low, Japan's PMI Accelerates in May

U.K. consumer price inflation dropped to 8.7% in April, the lowest since March 2022, primarily due to a slowdown in electricity and gas prices. However, the rate exceeded expectations and remained well above the Bank of England's target of 2.0%. Housing & utilities inflation declined sharply to 12.3%, while inflation in sectors like restaurants & hotels and furniture, household equipment & maintenance also eased. Food & non-alcoholic beverages inflation remained near record highs, while transportation, recreation & culture, and miscellaneous goods & services experienced price increases. The core inflation rate, excluding food and energy, rose to 6.8%, the highest since March 1992.

The Eurozone Composite PMI dropped to 53.3 in May, marking a three-month low and falling below market expectations. Despite the fifth consecutive month of expansion in private sector activity, manufacturing contracted faster while the services sector showed resilience. Demand growth slowed, leading to output surpassing new orders at a level not seen since 2009. Employment growth slowed, and average prices rose at the slowest pace in 25 months. Concerns over weaker customer demand and higher interest rates contributed to declining optimism about the future. The data suggests uneven economic growth in the Eurozone during the second quarter.

Japan's au Jibun Bank Flash Composite PMI rose to 54.9 in May 2023, the highest since October 2013, signaling the fourth consecutive month of private sector growth. Service providers saw strong expansion, setting a record increase in business activity, while manufacturers experienced improvement for the first time in seven months. Employment levels rose solidly, and input prices increased at a slower pace. Confidence remained robust despite a slight easing from the previous month.

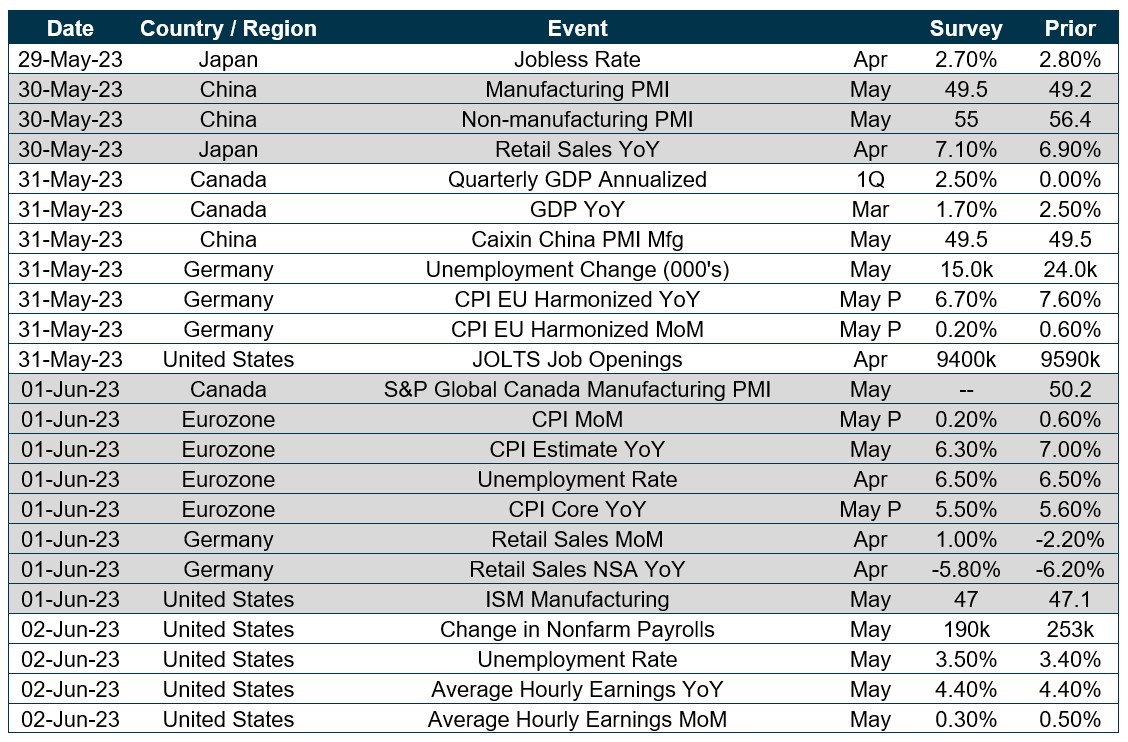

Quick look ahead

As of May 26, 2023