Weekly Market Pulse - Week ending June 21, 2024

Market developments

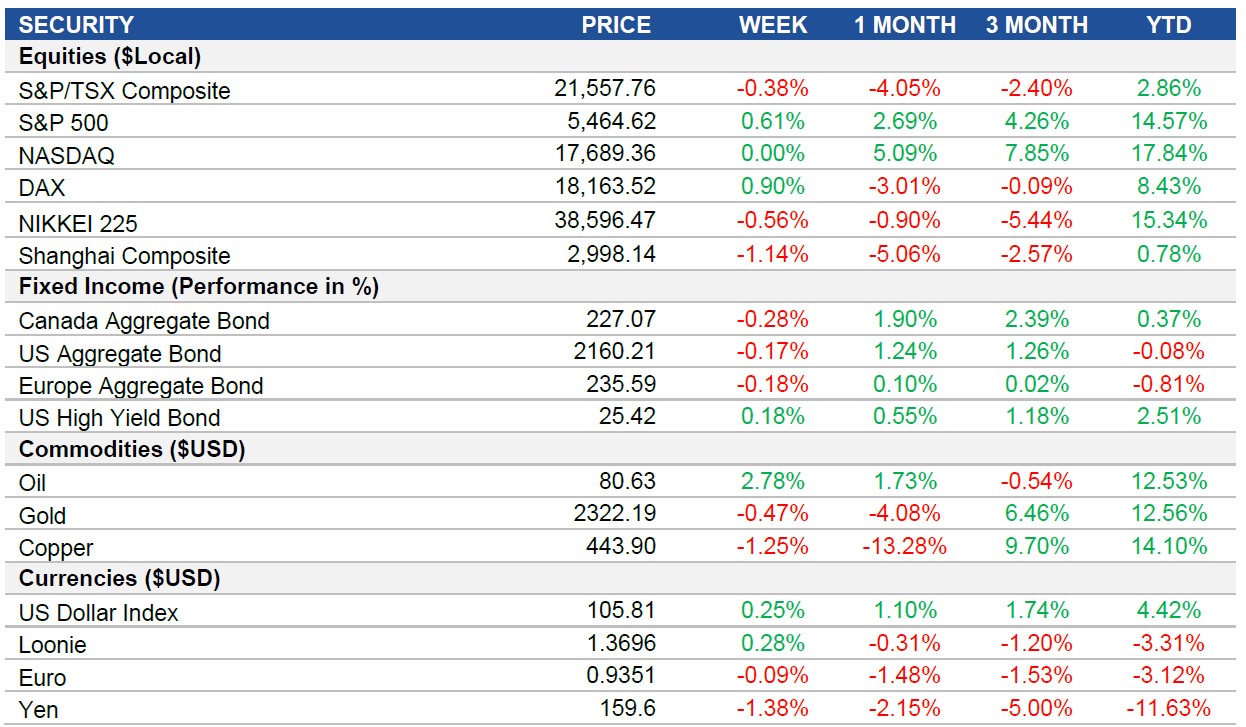

Equities: The U.S. markets experienced a significant options expiration event known as "triple witching," with an estimated $5.5 trillion in contracts set to expire. This event is causing volatility in the stock market, particularly affecting Nvidia, which holds the second-largest value of expiring contracts. Despite market turbulence, tech funds have seen record inflows driven mainly by the ongoing AI frenzy. However, there are growing concerns about equity concentration risk, especially in AI-related stocks. With all the volatility this week, the S&P 500 Index ended up 0.60%, Nasdaq was flat, while the TSX was down 40bps.

Fixed Income: Risk-off trades gained favour at the end of the week, influenced by political uncertainty in France following President Macron's call for a snap election. Market expectations indicate a second ECB rate cut by October and an 80% chance of a third cut this year. As such, traders are adjusting their expectations for Federal Reserve policy, now pricing in about two quarter-point rate cuts this year, with the first one fully expected in November.

Commodities: Oil futures also ended lower on Friday, but still managed to achieve a significant weekly gain. The weekly gain in oil prices was primarily driven by investors assessing the risk of a broader conflict in the Middle East, which could potentially disrupt crude oil supply from the region.

Performance (price return)

Source: Bloomberg, as of June 21, 2024

Macro developments

Canada – Steep Decline in Canadian Retail Sales

Retail sales in Canada are projected to have dropped by 0.6% in May 2024, marking the steepest decline since March 2023. This drop offsets April's 0.7% surge, driven by a significant increase in gas station sales. Despite the overall drop, core retail sales in April surged by 1.4%, led by grocery and sporting goods stores.

U.S. – U.S. Retail Sales Show Slight Increase Amid Cooling Consumer Sentiment, U.S. Composite PMI Hits Highest Level Since 2022

U.S. retail sales edged up 0.1% in May 2024, following a revised 0.2% decline in April, indicating cooling consumer sentiment. Significant increases were seen in sporting goods and motor vehicle sales, while gasoline and furniture sales declined. Excluding gasoline, sales rose 0.3%, contributing to a 0.4% increase in GDP-related retail metrics.

The S&P Global U.S. Composite PMI rose to 54.6 in June 2024, the highest since April 2022. The service sector showed significant improvement, while manufacturing growth slowed slightly. Business confidence and demand growth led to workforce expansion, and decreased input cost growth indicated moderating inflationary pressures.

International – U.K. Inflation Slows to Target Rate, Bank of England Maintains Interest Rate Amid Balanced Decision, Eurozone Composite PMI Declines Amid Manufacturing Contraction, Eurozone Services Sector Growth Slows, Japan's Inflation Rate Hits Highest Level Since February, China’s Retail Sales Growth Accelerates

The U.K. inflation rate slowed to 2% in May 2024, the lowest since July 2021, aligning with the Bank of England's target. The slowdown was driven by reduced food costs and eased prices in various sectors, despite a slight acceleration in transport costs. Core inflation also eased to 3.5%.

The Bank of England maintained its interest rate at 5.25% during its June meeting. Despite calls for a rate cut by some policymakers, the decision reflects ongoing concerns about inflationary pressures and a commitment to restrictive monetary policy until inflation risks diminish sustainably.

The Eurozone Composite PMI fell to 50.8 in June 2024, reflecting slower growth in private economic activity. The services sector continued to expand, offsetting a deeper contraction in manufacturing. New orders contracted due to low export demand, while input cost inflation hit its lowest level this year.

Japan's annual inflation rate accelerated to 2.8% in May 2024, the highest since February, driven by a steep rise in electricity prices and increased costs in various sectors. Core inflation rose to 2.5%, and the monthly CPI saw its largest increase since October 2023.

China's retail sales grew by 3.7% year-on-year in May 2024, the sharpest rise since February. Significant growth was seen in home appliances, personal care, and communications equipment. Monthly retail trade increased by 0.51%, marking the most substantial rise since October 2023.

Quick look ahead

As of June 21, 2024