Weekly Market Pulse - Week ending March 3, 2023

Market developments

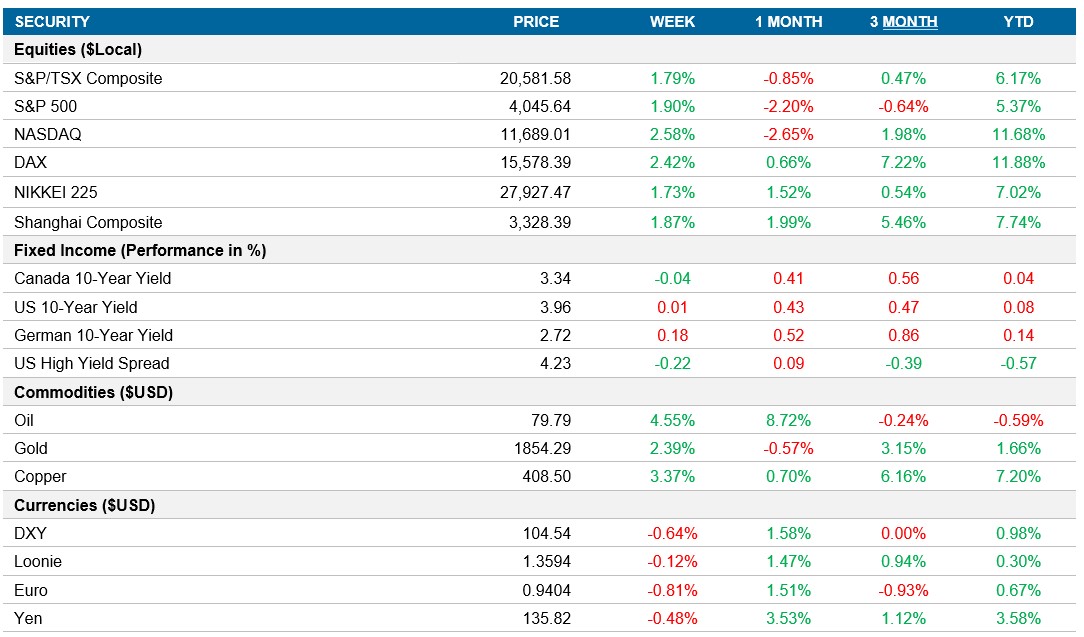

Equities: The U.S. market bounced back after a difficult week last week as investors speculate that the Fed won’t raise rates above the peak rates that are currently being priced in. The S&P finished the week up nearly 2% and the Nasdaq around 2.6% even as a jobs report showed continued strength in the labour market as investors believe the impact from the Fed’s tightening cycle takes time to be reflected in the data. Markets in Europe and Asia ended the week higher as well and China recovered some of the losses from last month as positive economic data drove markets higher.

Fixed income: The U.S.10yr rate finished the week relatively unchanged at 3.96%, as the bond market rallied on Friday. The start of the week saw a selloff in the bond market and led to the whole curve crossing the 4% mark on Thursday. The market is currently pricing in peak rates of ~5.5% and is expected to remain higher for longer.

Commodities: Oil closed higher on Friday after falling on reports that the U.A.E were discussing leaving OPEC were denied. Following the flat performance last week, Oil closed +4.5% as strong economic data from China outweighed the worries in the U.S that the Fed may need to raise rates above what was previously expected.

Performance (price return)

As of March 3, 2023

Macro developments

Canada – Q4 GDP was unchanged, missing expectations of a 1.6% expansion

The Canadian economy stalled in Q4, after five consecutive quarters of growth. Inventory accumulation declined for manufacturing and retail goods, leading investment in inventories to decline. Higher interest rates pressured investment in housing. On the other hand, consumption expanded in the quarter driven by both household and government. The 0% change in Q4 GDP leaves the economy in worse shape than the Bank of Canada expected.

U.S. – ISM Manufacturing falls short of expectations and ISM Services comes in at 50.6

ISM Manufacturing PMI moved slightly higher to 47.7 in February, up from 47.4 a month ago but missing expectations of 48. This was the fourth consecutive month of falling factory activity as outputs continue to slow to match demand.

Services PMI came in at 50.6 in February, almost in line with the preliminary reading and an uptick from the 46.8 in January. As inflationary pressures persist and interest remain high, new business declined at the slowest pace since October. On the price side, input cost inflation was the second slowest since October 2020.

International – Eurozone CPI was above expectations at 8.5% and the unemployment rate remains near the lows at 6.7%, China Composite PMI jumped to 54.2, Retail sales in Japan beat expectations

Eurozone CPI moved lower to 8.5% in February, marking the lowest reading since May, but above market expectations of 8.2%. The data signaled that inflationary pressure remained elevated and we can expect the ECB to remain hawkish. Within the largest economies in Europe, we saw inflation accelerate in Germany, France, Spain, and the Netherlands. Core inflation (excluding food and energy) hit a record high of 5.6% in February.

Eurozone unemployment rate stayed at 6.7% in January, unchanged from December and a touch higher than market expectations of 6.6%. The jobless rate remains close to the record low seen in October of 6.6%.

China Composite PMI climbed to 54.2 in February, up from 51.1 a month ago. This was the second consecutive period of growth and the strongest since last June, driven by the reopening of the economy. The reopening led to confidence staying at the decade high we saw in January.

Retail sales in Japan jumped by 6.3%, well ahead of market forecasts of 4.0% and above the 3.8% a month ago.

Quick look ahead

As of March 3, 2023