Weekly Market Pulse - Week ending May 31, 2024

Market developments

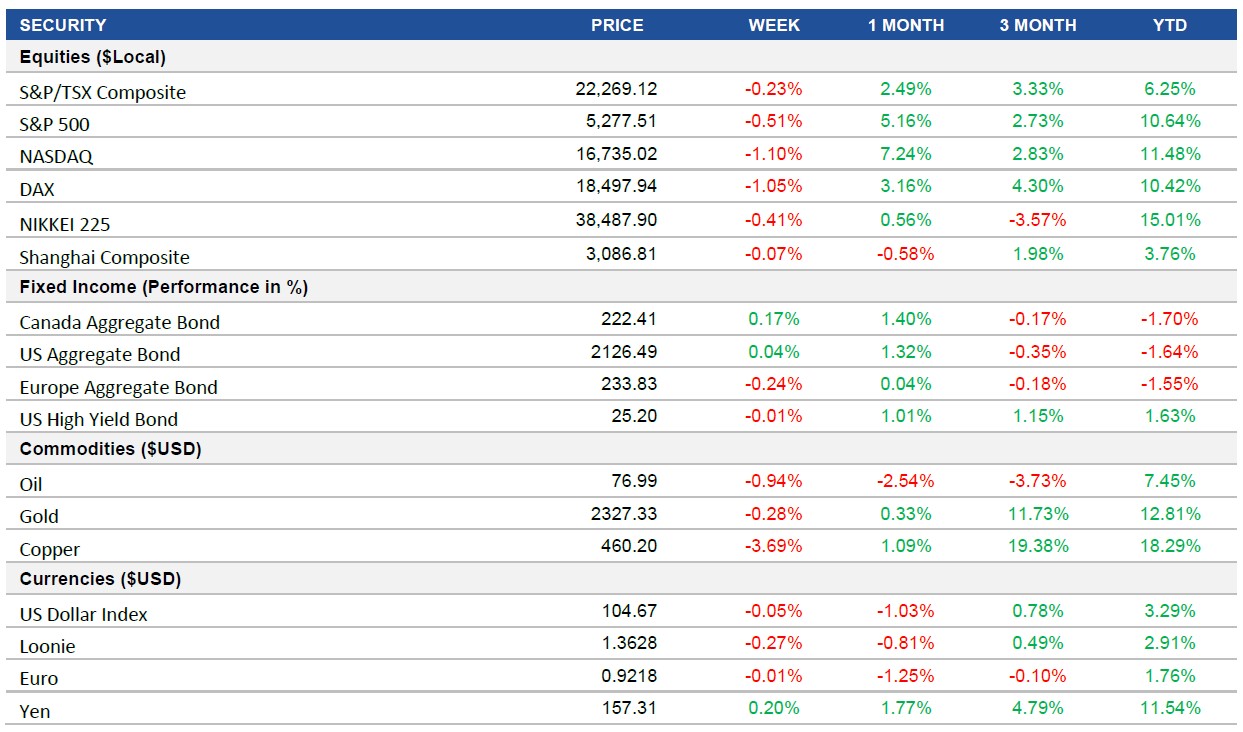

Equities: Technology stocks tumbled, dragging down the broader market and trimming the monthly rally fueled by hopes of Fed rate cuts. As inflation cools, interest rate cuts could provide a tailwind for growth-oriented tech stocks by boosting cash flows for investments and acquisitions. AI, cloud computing, and 5G trends are also driving demand in parts of the tech sector. The TSX also closed lower this week as Bank of Montreal earnings missed analyst estimates, offsetting the stronger report and performance of Royal Bank of Canada.

Fixed Income: U.S. treasuries had their best month of 2024 as the price gage for personal consumption expenditures came in line with expectations. The Fed will likely need to see more consistent favourable data before initiating the first rate cut and traders are currently pricing in a 50% probability for that to happen by mid September. The Bank of Canada and ECB are likely to begin easing earlier than the U.S., as the market is expecting the announcement of the first rate cut to come as early as next week.

Commodities: Oil prices fell for the third consecutive day on Friday and closed lower for the week. This decline occurred despite the U.S. inflation data meeting expectations, as the market awaits the OPEC+ meeting this weekend where production cuts are expected to be extended into the third quarter or beyond.

Performance (price return)

Source: Bloomberg, as of May 31, 2024

Macro developments

Canada – Canadian Economic Growth Comes in Below Expectations

The Canadian economy expanded by 0.4% in Q1 2024, primarily driven by a 0.7% increase in household spending, especially on services. Imports and exports both increased modestly, while business capital investment grew by 0.8%, particularly in the oil and gas sector. Annual GDP growth was 1.7%, below market expectations of 2.2%.

U.S. – U.S. Economic Performance Impacted by Consumer Slowdown, Persistent Inflation and Weaker Consumption Outlook in the U.S.

The U.S. economy grew at an annualized rate of 1.3% in Q1 2024, revised down from earlier estimates and significantly lower than Q4's 3.4% growth. This was due to a larger than expected slowdown in consumer spending. Revisions showed mixed results in investment and government spending, with some areas performing better and others worse than initial estimate.

April's PCE deflator data indicated ongoing inflation above target, though slightly improved from early 2024. Core PCE inflation remained steady at 2.8%, with a minor increase in certain service prices offset by declines in others. The data suggests potential weakening in Q2 consumption growth.

International – Eurozone Unemployment Hits Record Low, Rising Inflation in the Eurozone, Japan's Retail Sales Growth in April

The Eurozone's unemployment rate dropped to a record low of 6.4% in April 2024, with significant decreases in youth unemployment. Spain continued to have the highest unemployment rate, while Germany had the lowest. The overall jobless rate was slightly higher than a year earlier at 6.5%.

The annual inflation rate in the Eurozone rose to 2.6% in May 2024, the first increase in five months, exceeding forecasts. Energy prices rebounded and service prices increased, while inflation for food, alcohol, tobacco, and non-energy goods slowed. Core inflation also rose to 2.9%, higher than expected.

Japan's retail sales grew by 2.4% year-on-year in April 2024, accelerating from March and exceeding market forecasts. The growth was driven by increased sales in machinery, non-store retail trade, and pharmaceuticals. However, automobile sales and textile/clothing sales declined. Monthly sales rebounded by 1.2% from a fall in March.

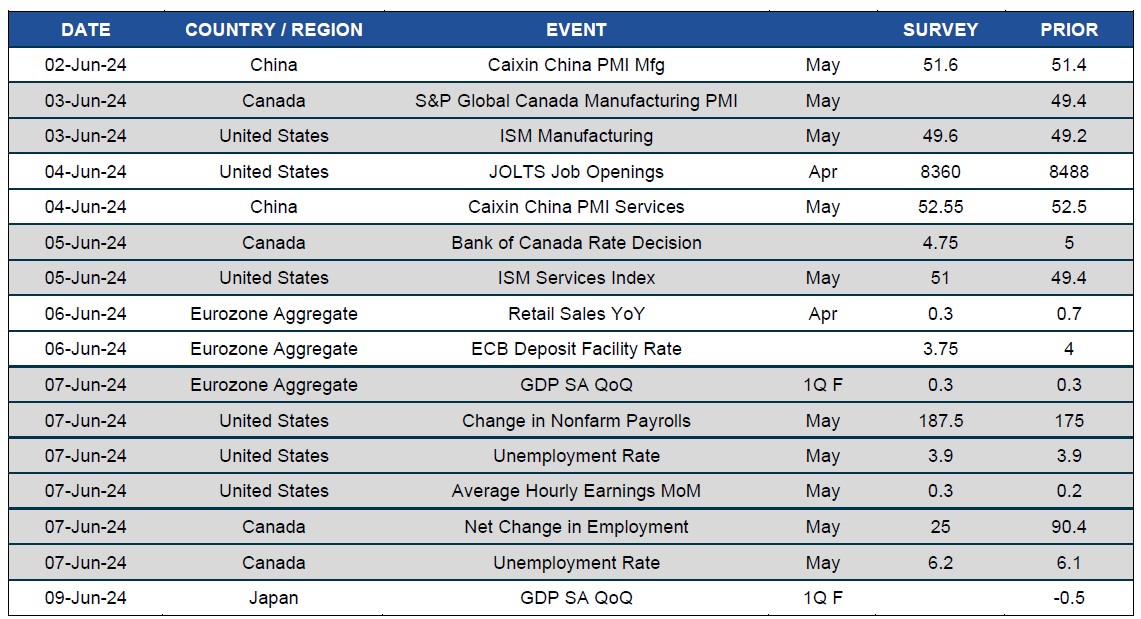

Quick look ahead

As of May 31, 2024