The new kings of the bond market

By Joe Rennison in London, Robert Armstrong in New York and Robin Wigglesworth in Oslo | janvier 21, 2020

When Josh Barrickman became known as the new “bond king”, his colleagues teased the taciturn fund manager by leaving paper crowns from Burger King at his desk.

The low-key Ohio native may not have the high profile of bond market stars such as Bill Gross but he has earned his title. The fund he runs, the Vanguard Total Bond Market, is the world’s biggest fixed income fund, with $247bn in assets under management.

The fund’s table-topping position exemplifies the revolution under way in the $9tn US bond market. Unlike the freewheeling, actively-managed Total Return fund once run by Mr Gross, Vanguard’s flagship bond fund is a passive, index-tracking fund. It takes a smaller fee from investors and tries to track the market, not beat it.

Exchange traded funds, which also strive to mimic an underlying benchmark but trade like a stock, have helped popularise passive investing. In equities they have become huge, but they are catching on in fixed income as well. Last year, the assets in passive bond ETFs hit $1tn for the first time, according to data provider ETFGI.

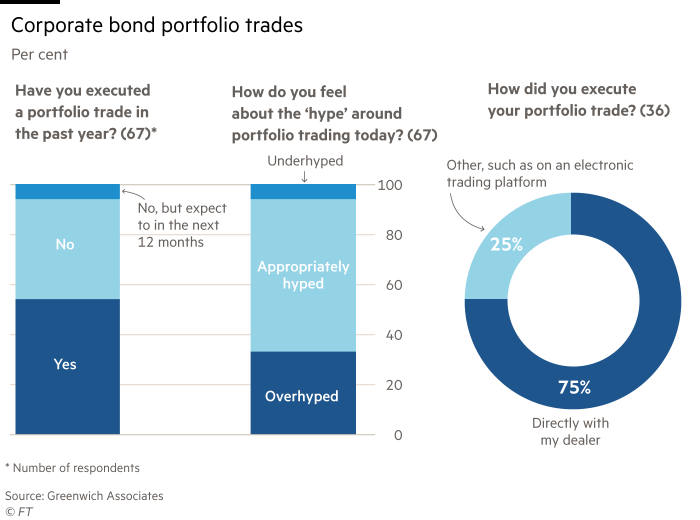

Such a radical shift has been facilitated by big changes in trading technology. Gone are the clunky Telex machines traders forcefully punched transactions into. Now hundreds of bond trades can be electronically priced as one and executed simultaneously with a single counterparty. This new form of “portfolio trading”has spread from ETFs, taking hold across Wall Street and working its way back to investors like Mr Barrickman.

“ETFs on the fixed income side are a really big deal,” he says. “For fixed income this is really our first exchange-traded, liquid and transparent market. They lend themselves perfectly to the portfolio trading phenomenon.”

It has also drawn a whole new class of players into the market. Bond trading was once the highly lucrative domain of investment banks — from the heyday of Salomon Brothers in the 1980s to Goldman Sachs’ high-octane business of the past two decades. But now a new generation of lightning-fast, computer-savvy trading firms is providing alternative places for fund managers to trade.

“We are on the verge of some of the biggest changes in this landscape for decades,” says Matt King, a strategist at Citi.

Just over four years ago Matheus Pereira was taking his final exams at the prestigious Wharton business school at the University of Pennsylvania. Today, working in the New York office of a Dutch high-frequency trading firm, the Brazilian reckons he is responsible for 3 per cent of US high-yield bond trading volume. Some days, he says, his firm’s trading accounts for 10 per cent of the market. He is 28 years old.

Mr Pereira’s meteoric rise has been made possible by the shift towards passive investing and fixed-income ETFs. He joined his firm, Flow Traders, in July 2015 and took over as head of trading a year ago. He has never worked at a bank and never traded with a Telex machine.

Mr Pereira says a lack of familiarity with old systems is liberating. He likens the bond market to the “marshmallow challenge” created by designer Peter Skillman: a team has to quickly create the tallest structure they can that will support a marshmallow, using 20 pieces of spaghetti, a metre of tape and a piece of string. Pre-school children consistently beat business school graduates, lawyers and executives.

“They [the children] are not thinking about the rules of physics and what is logical,” he says. “They are really just trying to think of what works.”

The bond market innovators take a similar approach. Flow Traders, along with rivals such as Jane Street Capital and Susquehanna International, makes markets in ETFs, offering investors a price to buy or sell shares. In fixed income markets, ETFs are created by exchanging a basket of bonds — usually 100 or so — with an ETF provider for a set number of ETF shares that can then be traded like a single stock. Conversely, the shares can be redeemed for the underlying bonds.

Through this “creation and redemption” process, market-makers like Flow Traders end up trading not just in the ETF but also in the underlying corporate bond market. As money poured into ETFs, the volume of trading by the new players grew.

It laid the foundation for the rise of portfolio trading, with the ability to trade multiple bonds simultaneously taking on a new importance, not least for the banks eager to hoover up the emerging business.

But it presented challenges. How do traders assess the value of hundreds of individual bonds and reduce them down to one tradeable price? The answer, again, is through technology — harvesting data from regulatory reported bond trades and ETF prices listed on exchanges.

Even before the rise of fixed income ETFs in recent years, there has been a slow move toward electronic bond trading, which has increased the amount of public price information. Now, electronic platforms like MarketAxess and Tradeweb collectively account for 34 per cent of all higher-rated, investment grade corporate bond trades.

With more available information, trading platforms, along with other data companies, have begun producing composite, indicative prices for a range of bonds. Banks and trading firms have also developed their own models to electronically price securities, often using the third-party prices as an input.

“The evolution taking place in credit — with ETFs at the centre — is about third-party pricing,” says Jon Klein, head of US investment grade and head of US macro credit products at Bank of America. “There is a growing comfort to using third party prices that is changing the face of credit.”

It means an Excel spreadsheet filled with tens, or even hundreds, of different bonds can be priced in minutes. Bank of America says it can price a portfolio of 100 bonds in five minutes, with even the trickiest trades typically priced in under one hour. Other banks give similar timeframes.

Jane Street says the size of a single portfolio trade can range from 10 to 1,000 different bonds, adding up to over $1bn. Over the course of 2019 Jane Street completed $66bn in credit portfolio trades, up from just $12.5bn in the second half of 2018, when they started doing these transactions.

“Portfolio trading was just a very natural extension of the business that we were doing,” says Matt Berger, head of fixed income trading at Jane Street. “It’s not a totally new idea, but started becoming a daily occurrence last year.”

As banks have responded by building out specialised portfolio trading businesses, the practice has expanded to other clients. Cash-strapped fund managers have been attracted by the prospect of trading a slew of bonds at once in an attempt to cut costs.

“Two years ago pricing 800 bonds would be an all-hands-on-deck, all-day exercise. Now it can be done in minutes,” says Dan Veiner, global head of fixed-income trading at BlackRock.

The emergence of portfolio trading could even address one of the biggest financial stability concerns to emerge over the past decade.

Traditionally, when asset managers have suffered investor withdrawals, they had little choice but to raise cash quickly by selling their most liquid bonds. That could push prices lower and made funds’ portfolios riskier, exacerbating investor fears and driving further withdrawals.

Last summer Mark Carney, the Bank of England’s governor, told a parliamentary committee that funds which promised investors that they can withdraw money at any time while investing in rarely-traded securities — such as many corporate bonds — were “built on a lie”, and that the risks “could be systemic”.

Portfolio trading offers a possible solution. Instead of selling a large amount of one bond, an asset manager could quickly sell a small amount of a lot of bonds, with the portfolio they own afterward looking much like the initial one, only smaller. This could ease concerns over a downward spiral into illiquidity, argues Citi’s Mr King.

“We do not see this resolving all the systemic concerns, especially where investor herding is concerned,” he says. “But at a minimum, we think this has the potential to revolutionise how individual portfolio managers think about day-to-day liquidity management.”

Banks are fighting to keep up with the industry by investing in electronic infrastructure. Their sense of urgency is underlined by the fact that most of them claim to be a “market leader” or “innovator” in electronic or portfolio trading of bonds.

Some bankers wonder whether what is happening in bond markets will echo what happened to equities trading. As that market digitised, the volume of trades skyrocketed, but the profit margin on each trade compressed. More and more of the trading profits went to the handful of firms with the biggest market share. Plain vanilla cash trading of equities, as opposed to trading of derivatives or other complex products, has become an unattractive business for the banks and shifted to new players.

Bond trading, similarly, seems likely to become more of a scale game, and total trading profit for the industry will fall, say analysts, even as the very largest players prosper.

“One thing that we all know is that once you have machines providing the services, the ability to scale capacity on the sell side over some relatively short timeframe is limitless,” says Phil Allison, head of fixed income automated trading at Morgan Stanley. “The inevitable outcome of that is undoubtedly some degree of margin compression.”

At the same time, banks’ stranglehold on the industry is starting to loosen. High-frequency trading firms that first came to the banks as customers are finding new ways to trade on electronic bond platforms, in some cases connecting directly with the banks’ client base of asset managers and hedge funds.

Tradeweb saw quarterly portfolio trading volumes on its platform rise from $2.7bn after it launched the service in the first quarter of 2019, to almost $18bn in the final three months of the year. MarketAxess, the largest US electronic corporate bond trading platform, says one of its top customers on its new Open Trading venue, where anyone can trade with everyone, is Jane Street, highlighting the importance of these new firms.

Joe Geraci, co-head of spread products at Citi, says that if high-speed trading firms continue to increase their presence in corporate bond trading, bid-ask spreads on the biggest, most liquid bonds (the key constituents of ETFs) will go down. Compressed spreads will probably put pressure on the profitability of bank trading desks. Business models will probably need to adjust.

There is a lot of money at stake. Industry insiders say that between a fifth and a third of banks’ “Ficc” (fixed income, currency and commodity) trading revenue comes from corporate bond trading. And Ficc trading revenues at the top five players — JPMorgan, Citgroup, Bank of America, Goldman Sachs and Morgan Stanley — totalled over $48bn in 2019.

Bank clients would be happy if spreads narrow — it would mean they were paying less to trade. But some participants say there are other factors to be mindful of.

The advent of new technology brings with it the possibility of new risks. While some bankers profess portfolio trading will make it easier to buy and sell even the most unloved bonds, others say that those that do not fit neatly into the big ETFs, particularly those of smaller issuing companies, might see their debt shunned. If this happened, it could mean that the bonds would trade at a discount, driving up the small companies’ cost of funding.

“We could see a growing bifurcation between securities that are deliverable in ETF baskets and [those that are] not,” says Mr Geraci.

Another worry is that confidence in third-party pricing could give way to complacency. A valuation created from out-of-date or inaccurate data could quickly become cemented in the market by unquestioning trading activity, only to rapidly unravel once discovered. “There is the potential for an echo chamber for illiquid bonds,” says Sonali Theisen, head of fixed income market structure and electronic trading at Bank of America.

Finally, there is the concern that electronification makes markets vulnerable to sudden bursts of volatility that traders cannot foresee and struggle to contain. “Every electronic market has been through some flash crash type event,” says one bank executive. “The cycle speed of the computers is so much quicker than humans.”

Bankers, trading platforms and asset managers say they have safeguards to protect themselves but the possibility of unforeseen glitches remains.

“The good news with that is we have a blueprint of how to avoid that with the equity market,” says BlackRock’s Mr Veiner.

This article was updated on January 22 to make clear Jane Street completed $12.5bn in credit portfolio trades in the second half of 2018, not last year

© The Financial Times Limited 2020. Tous droits réservés.

Veuillez ne pas copier-coller les articles du FT pour les distribuer par courriel ou les publier sur le Web.