How sequential risk can impact your retirement savings

Table of contents

Key takeaways

- Sequential risk is the potential impact of a significant market downturn during the early years of retirement, at a time when you need to draw an income from investments.

- Investment returns early in retirement affect a larger pool of money, which means that above-average gains/losses early on are amplified in later years.

- Sequential risk can be contained or managed if investors avoid playing it too safe or being overly aggressive with asset allocation strategy.

Related articles

- Five types of investment risk

- Seven strategies to help manage volatility and risk

- The importance of setting financial goals

- What is asset allocation?

What is sequential risk?

Sequence of returns risk (or "sequential risk") is the potential impact of a significant market downturn during the early years of retirement, at a time when you need to draw an income from your investments.

The returns you earn during the first few years of retirement are particularly important. Above-average returns can allow savings to last longer and support a higher income stream. But above-average losses can be hard to recover from. The reduced savings might not last as long as planned, potentially requiring you to live on a lower income.

The potential impact of sequential risk

Sequential risk emerges once you start drawing a regular income stream from your portfolio. Because the draw-down tends to reduce the asset base over time, investment returns early in retirement affect a larger pool of money. In effect, above-average gains or losses early on are amplified in the years ahead.

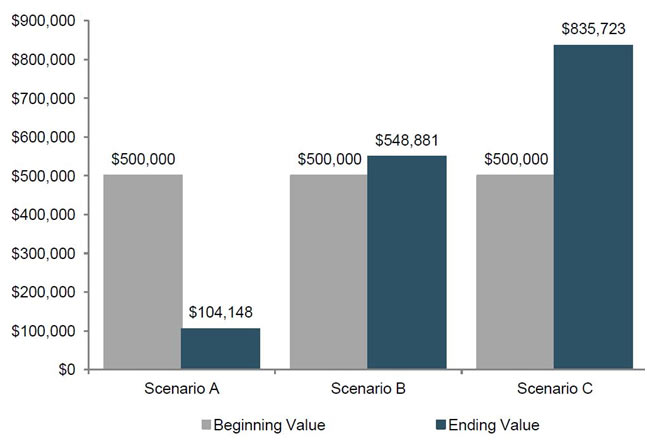

A simple example illustrates how sequential risk can affect retirement savings.

- Imagine a hypothetical retiree who starts retirement with a portfolio value of $500,000.

- Over 30 years, they earn an average return of 5.4%, and they withdraw an income of $21,000 per year (indexed for inflation of 2% in this example).

- Compare that scenario to two variations featuring an above-average gain or loss in the first year versus the last year of retirement.

| Scenario A | Scenario B | Scenario C | |

|---|---|---|---|

| Starting balance | $500,000 | $500,000 | $500,000 |

| Annual withdrawal amount (indexed at 2%) | $21,000 | $21,000 | $21,000 |

| Return year 1 | -15% | 5.4% | 27% |

| Return year 2 to 29 | 5.4% | 5.4% | 5.4% |

| Return year 30 | 27% | 5.4% | -15% |

| Value at year 30 | $104,148 | $548,881 | $835,723 |

| Average return for 30 years | 5.4% | 5.4% | 5.4% |

Although all three scenarios produce an average return of 5.4%, you can see in scenarios A and C how dramatically an above-average gain or loss early in retirement can affect the savings.

How to reduce sequential risk

Fortunately, sequential risk can be contained or managed if you follow a few fundamental investing guidelines:

- Avoid being overly aggressive with your retirement savings portfolio — ensure that your asset allocation strategy is appropriate for your risk profile. For example, a balanced portfolio with 50% equity and 50% fixed income is likely to come through a market correction in better shape than an 80% equity portfolio.

- Avoid playing it too safe — too much emphasis on capital preservation can subject a portfolio to the "risk of no risk" where investment returns don't keep up with inflation, thereby gradually eroding the purchasing power of the savings.

- Be realistic about time horizons — Canadians are enjoying longer life spans. A typical retirement could last 20, 25 or even 30 years. That's why, especially early in retirement, it might make sense to maintain a balance of growth-oriented and income-oriented investments.

- Trust your plan — if you've decided that a particular asset allocation strategy is appropriate for your risk profile and long-term goals, then it's likely still appropriate after a short-term market correction. Long-term investors who react to short-term market movements by shifting assets often end up worse off than those who simply stay the course.

The information contained in this article was obtained from sources believed to be reliable; however, we cannot guarantee that it is accurate or complete. This material is for informational and educational purposes and it is not intended to provide specific advice including, without limitation, investment, financial, tax or similar matters.