Weekly Market Pulse - Week ending June 17, 2022

Market developments

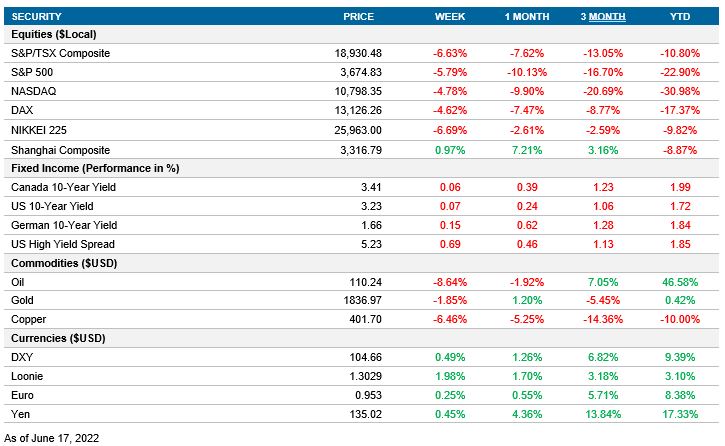

Equities

U.S. equities were down for the third week in a row. The S&P 500 Index recorded its biggest weekly drop since the pandemic decline in March 2020. Investor concerns have been exacerbated by aggressive central bank actions to tamp down inflation, and the possibility that these actions could push economies into a recession. China managed to stay relatively positive, though there are concerns due to parts of Shanghai resuming lockdown measures.

Fixed income

Yields increased after the U.S. Federal Reserve instituted its biggest rate hike since 1994. Bond investors’ concerns remain with the magnitude and persistence of high inflation. High-yield spreads widened during the week as the impact of higher rates on corporate credit risk escalated.

Commodities

Markets entered an uncharacteristic slump this week due to concerns of a potential near-term recession decreasing demand. Oil prices are at a three-week low and copper prices dropped for the second consecutive week. The price of gold dropped in sync with rising yields

Performance (price return)

As of June 17, 2022

Macro developments

Canada – Manufacturing sales rise; Housing starts increase; Wholesale sales contract

StatsCan released the manufacturing sales data for April. Month-over-month manufacturing sales growth met consensus estimates of 1.7%. This is the seventh consecutive increase in manufacturing sales. Increases in carbon fuel products (3.7%) and transportation equipment (6.4%) led the charge. Additionally, inventory (2.3%) and unfilled orders (2.9%) continued to rise during April.

CMHC released its housing starts data for May. The seasonally adjusted annual rate for housing starts was 287K units, up from 267K the previous month—an increase of 8.0%. Economists estimated housing starts to be 255K. This is the second month in a row that the housing starts release managed to beat expectations. Urban housing starts also reported an 8% increase, reaching 264K units. This increase is attributed to the higher number of multi-unit starts in urban areas.

StatsCan’s wholesales sales data release for April came in below expectations. Declines in motor vehicle (-1.5%), agricultural supply (-13.6%), and lumber (-3.8%) sales were primary factors. It should be noted that whilst motor vehicle sales have declined throughout North America, this is more of a supply chain issue stemming from Asia rather than a global demand issue. Tobacco products (-17.3%) and cannabis (-8.4%) also performed poorly, but these did not make as much of an impact due to the small size of these industries within the basket. Interestingly, home entertainment equipment sales grew by 7.1%.

U.S. – PPI rises; Retail sales contract; Empire manufacturing index falls; Fed hikes rates 75 bps; Housing starts fall

The U.S. Department of Labor released May’s Producer Price Index data. Final demand increased 0.8% month over month, meeting expectations. This increase can be attributed to the increase in demand for energy goods, which rose 5.0% month over month. Core PPI (excluding food and energy) increased 0.5% month over month, slightly below expectations. Year-over-year PPI readings were below expectations. Final demand rose 10.8% and core PPI rose 8.3% year over year.

The Census Bureau reported May’s retail sales. Sales failed to meet expectations and contracted 0.3%. The contraction was driven by a decline in automobile sales (-3.5%). This was offset by growth in the sale of food and beverage products (1.2%). It is also notable that the restaurant industry managed to expand for a fourth consecutive month—growing by 0.7%, though growth here is starting to flatten.

The Federal Reserve Bank of New York released its Empire Manufacturing Survey for June. The index outlining general business conditions rose from -11.6 to -1.2. Prices paid and prices received both saw elevated readings, coming in at 78.6 and 43.6 respectively. Prices paid had a higher reading compared to May, when the reading was 73.7. In contrast, prices received had a lower reading than in May, when the reading was 45.6. What this suggests is that whilst manufacturers are continuing to receive higher payments for their goods, they are also paying higher input costs and that input costs are growing at a faster rate than revenue. Additionally, delivery times have continued their ongoing lengthening from 2021.

The Fed declared a rate hike of 75 bps to a 1.50%–1.75% target range on June 15. This was the largest rate hike since 1994. Citing the Ukraine-Russia conflict and supply disruptions from China as contributors to upward pressure on inflation, the Federal Open Market Committee reaffirmed its hawkish stance. The committee stated it is “strongly committed to returning inflation to its 2% objective.” Economists originally forecasted a 50-bp hike, but consensus slowly pivoted toward a 75-bp increase after the recent Consumer Price Index and PPI releases. Economic projections were revised downwards. Real GDP is projected to increase by 1.7% for year-end 2022 and 2023—down from earlier projections of 2.8% and 2.2%, respectively. The unemployment rate is expected to reach 4.1% by year-end 2024. Inflation is projected to be 5.2% for year-end 2022, up from the earlier forecast of 4.3%. The Federal Funds rate is expected to reach 3.4% for year-end 2022. The long-run projection for the Federal Funds rate was also revised upwards to 2.5%.

The Census Bureau also reported housing starts data. Housing starts in May had a sharp 14.4% decline from 1.81M units to 1.54M. This figure was well below consensus estimates of 1.69M and is also the lowest figure we have seen in 12 months. Whilst there is a healthy backlog of construction to be completed, new applications to build units have declined because of rising rates.

International – U.K. production disappoints; Chinese industrial production rises; Chinese retail sales fall; U.K. raises rates by 25 bps

The Office for National Statistics released the United Kingdom’s industrial and manufacturing production data for April. Industrial production fell 0.6% month over month. Industrial production contracted for every industry but energy, with energy seeing an increase of 0.1% month over month. The most significant detractor was the production of durable goods, which fell 4.6%.

The National Bureau of Statistics released China’s industrial production data for May. The consensus estimate was for Chinese industrial output to contract by 0.9%, but output managed to increase by 0.7%. The zero COVID policy did not have as harsh effects in May as expected, likely due to producers raising output in response to news that lockdowns would end on June 1. The largest growing category continues to be mining, which saw growth of 7.0%. The largest contribution to mining is the coal mining industry (8.2%), which stems from increased demand for carbon-based fuel products.

On the same day, the NBS released China’s retail sales data for May. The negative trend from March continues but figures managed to beat consensus estimates. In May, sales contracted by 6.7%. The previous month, sales fell by 11.1%. Food (12.3%), beverages (7.7%), medicine (10.8%), and gas (8.3%) sales continue to grow, but almost all other categories saw a loss in demand. The one exception is the tobacco and alcohol industry, which saw growth of 3.8% as consumers substituted service goods with leisure goods due to lockdown measures. Though lockdown measures were mostly lifted on June 1, there are parts of Shanghai reentering lockdown due to new COVID cases.

The Bank of England declared a 25-bp rate hike to 1.25%. Within their announcement, the BoE declared it is becoming more hawkish, or concerned with moderating inflation and aiding price stability. All members now agree that some form of quantitative tightening is now necessary. The BoE also stated that they are willing to “act forcefully in response to higher inflationary pressures if necessary.” Currently, the primary driver behind inflation is the rising cost of energy but the tight labour market is starting to prove a hindrance. Pay growth is strong and may end up acting as a barrier to moderating down to the BoE’s 2.0% inflation target.

Quick look ahead

Canada – Retail sales (June 21); CPI (June 22)

StatsCan will release retail sales for April. In March, retail sales were flat. However, that is largely due to the negative influence of automobiles, which is why core retail sales saw a small 1.5% increase. Economists are expecting retail sales to have grown by 0.8% in April.

The CPI release will occur the following day. Despite the Bank of Canada’s hawkish stance, April’s inflation data reported an increase, prompting the BoC to commit to its 50-bp hike. During the last interest rate meeting, the BoC insinuated that it is willing to act forcefully in order to meet inflation targets. Traders will be closely watching the CPI release in an attempt to determine if the BoC would be willing to commit to a more aggressive stance—potentially with a 75-bp hike. Currently, the consensus expectation is for inflation to have increased to 7.3% year over year in May.

U.S. – PMI (June 23)

S&P Global will release the IHS Markit Flash U.S. Purchasing Managers’ Index for June. Rising inflation and interest rates will likely hamper the manufacturing PMI. In May, the PMIs declined after a strong preliminary reading for these reasons, causing buyers to defer consumption to future periods. Economists are predicting a decrease in the manufacturing PMI to 56.3 and an increase in the services PMI to 53.5.

International – U.K. CPI (June 22); Japan’s PMI (June 22); Eurozone PMI (June 23); Germany’s PMI (June 23); Japan’s CPI (June 23); Germany’s ifo survey (June 24)

The Office for National Statistics will release U.K. inflation data for April. In March, the U.K. had a high inflation reading of 9.0% year over year. Economists expect inflation to increase to 9.2% year over year.

S&P Global will release Japan’s au Jibun Bank Flash PMI for June. The next day, IHS Markit Flash PMIs for the aggregate eurozone and Germany will be released. The European PMI releases are expected to report a slight decrease from their May figures.

The Statistics Bureau of Japan will publish May’s CPI data. Inflation is expected to stay flat at 2.5% year over year. For the last three months, Japan’s inflation data have been consistently matching consensus estimates. In April, the main drivers of inflation were food and utilities, which is a trend that started near the end of 2021.

Germany’s ifo Institute will release its business climate index for May. The April release managed to beat estimates, with a reading of 93.0. In April, German industrial production was helped by pent-up demand. We may see lower expectations stemming from declining new orders and rising inflation costs. Economists are forecasting a decrease in the business climate index to 92.0.