Weekly Market Pulse - Week ending August 19, 2022

Market developments

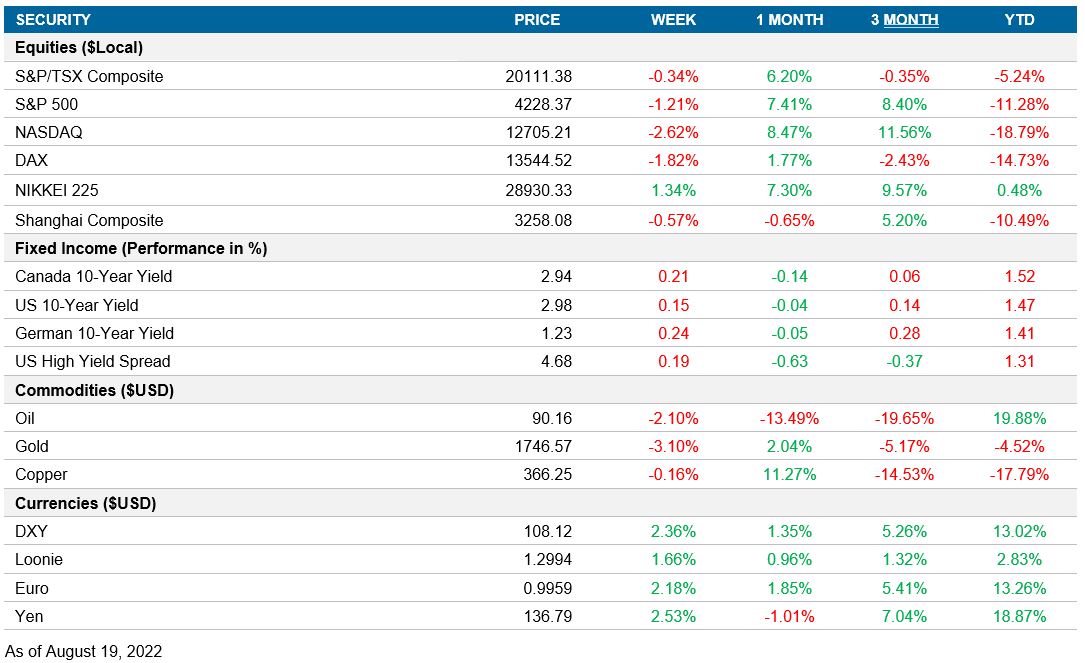

Equities: Investor sentiment weakened after the Federal Reserve signaled further rate hikes in their July minutes. Equities broke their four-week winning streak as markets turned negative in the latter half of the week.

Fixed income: U.S. yields rose as a result of a sell-off of less risky assets. The U.S. yield curve slightly flattened but the 10 and 2-year yields remain inverted.

Commodities: Oil prices fell alongside investor sentiment as fears of a recession increased. Copper prices also fell but this was offset by the People’s Bank of China quantitatively easing which increased copper demand in the region. Gold lost its momentum from last week as bonds rallied and investors believe inflation will fall further.

Performance (price return)

As of August 19, 2022

Macro developments

Canada – Manufacturing and wholesale sales weakens; Housing starts increases; CPI weakens; Retail sales rises

Canadian manufacturing sales had a weak release for the month of June. Manufacturing sales contracted by 0.8% month-over-month. The sales of petroleum products fell by 7.8% and sales of wood products fell by 7.2% month-over-month. However, motor vehicle sales increased 13.8% month-over-month. Similarly, wholesale sales also reported weak growth of 0.1% month-over-month.

Housing starts have remained strong for the fourth month in a row. July’s housing starts were 275K, up from 257K the month prior. This increase was due to rural starts which was around 21K. The number of urban starts declined by 0.8% to 254K, with multi-unit urban starts decreasing by 0.3% and single-detached urban starts decreasing by 2.3% month-over-month.

Canada’s Consumer Price Index released in-line with consensus estimates during July. CPI figures were 7.6% year-over-year and 0.1% month-over-month. The fall in inflation is attributed to a 9.2% month-over-month decrease in gasoline prices. However, the price of food continued to rise by 0.9% and shelter costs increased by 0.4% month-over-month. Wage growth is still lower than CPI, implying the Bank of Canada still has more room to tighten and may opt for a more hawkish 75-bp hike in September.

Canadian retail sales remained strong during the month of June. Reporting a sixth consecutive increase, retail sales surprised on the upside with readings of 11.0% year-over-year and 1.1% month-over-month. This was driven by a 3.9% increase in gasoline sales and a 1.8% month-over-month sales increase in the automobile industry. This was offset by a 1.1% month-over-month decrease in food and beverage sales as demand started to decline due to rising food prices. Core retail sales grew by 8.6% year-over-year and 0.2% month-over-month.

U.S. – Empire manufacturing index falls harshly; Housing starts decreases; Industrial production rises; Retail sales flattens

The Empire manufacturing index of general business conditions saw a harsh fall in August. Consensus estimates were for a reading of 5.0, but the actual reading was –31.3. New orders dropped by 35.8 points to –29.6 and unfilled orders dropped by 7.5 points to –12.7, representing a steady decline in demand. On the flipside, manufacturers have reported improved delivery times. Manufacturers are still hiring, but the pace is starting to slow, with the number of employees index falling by 10.6 points to 7.4. Business expectations for the next six months have improved with a reading of 2.1.

U.S. housing starts have continued to surprise on the downside for the fourth consecutive month in July. Housing starts had a reading of 1.45M, down from a revised figure of 1.60M in June. The decrease in housing starts was broad-based, with single unit starts declining by 10.1% and housing with five or more units declining by 10.0% month-over-month. Regionally, declines occurred throughout the United States aside from the Northeast region where starts increased to 230K up from 139K the previous month.

U.S. industrial production data for July came in above consensus estimates. Readings were 3.9% year-over-year and 0.6% month-over-month. The primary driver behind industrial production growth was a 0.7% month-over-month increase in manufacturing. The mining industry also posted a 0.7% month-over-month increase. These were offset by a 0.8% decrease in utilities production. Within market groups, increases were broad-based, and construction saw an increase of 0.9% month-over-month.

U.S. retail sales have started to show signs of weakening in July. Sales grew by 10.2% year-over-year but were flat month-over-month. Flat monthly sales can be attributed to lower gasoline prices since sales at the pump dropped by 1.8% month-over-month. However, gasoline still accounts for a 39.9% increase in yearly sales. Food sales increased by 8.4% year-over-year and 0.2% month-over-month.

International – Japan’s GDP rises; China’s industrial production weakens; U.K. CPI rises; Japan’s CPI rises; U.K. retail sales improves; German PPI rises sharply

Japan’s GDP estimates released below expectations for the second quarter. Japan escaped a technical recession with GDP readings of 0.5% quarter-over-quarter and 2.2% year-over-year. This expansion is attributed to a 1.1% quarter-over-quarter increase in private consumption. Residential investment continued its downwards trend, falling by 1.9% quarter-over-quarter.

China’s industrial production for July released below consensus estimates. Industrial production expanded by 3.8%, down from growth of 3.9% year-over-year in June. The slowdown in production stems from a slowdown in demand—Chinese retail sales also released below estimates. Global demand for goods produced in China such as iPhones are also seeing a decline, which is acting as an additional headwind.

U.K.’s CPI surprised on the upside as high energy prices continue to take its toll on the U.K.’s consumer. CPI readings were 10.1% year-over-year and 0.6% month-over-month. The price of housing/household services increased by 9.1% year-over-year and 0.4% month-over-month because of rising oil/gas prices. This is forecasted to further increase in October when Ofgem revises the energy price cap. Food prices increased by 12.7% year-over-year and 2.3% month-over-month as wheat supplies continue to stay tight from the ongoing Russia-Ukraine conflict.

Japan’s CPI met expectations during the month of July. CPI had readings of 2.6% year-over-year and 0.5% month-over-month. Core CPI had a reading of 2.4% year-over-year. Japan continued to handle its inflation situation well, with prices rising due to a weakening yen and tighter food supplies. The Bank of Japan will likely remain dovish for the near future despite inflation remaining above their 2.0% target.

U.K. retail sales had mixed readings for the month of July. Retail sales contracted by 3.4% year-over-year but increased by 0.3% month-over-month. The monthly figure was driven by a 0.7% month-over-month increase in online sales. This was offset by a 0.1% decrease in gasoline sales. Gasoline sales volumes declined by 0.9% month-over-month, with demand decreases caused by both inflation and an ongoing heatwave which discouraged consumers from travelling. The heatwave likely acted as a tailwind on online sales. Food sales remained unchanged on a month-over-month basis.

Germany’s Producer Price Index surprised on the upside with a sharp increase during the month of July. PPI readings were 37.2% year-over-year and 5.3% month-over-month. The primary driver of PPI continues to be energy, with prices increasing by 105.0% year-over-year and 14.7% month-over-month. The yearly PPI figure saw broad-based increases whereas the monthly figure had a slight offset in intermediate goods (-0.3% MoM) due to the declining price of metals.

Quick look ahead

Canada – No notable releases

No notable releases for the week.

U.S. – PMI (August 23); Durable goods (August 24)

IHS Markit will release their U.S. Flash PMI for August. In June, the manufacturing PMI was expansionary, but the services PMI was contractionary. There is a probability that the manufacturing PMI turns contractionary after the weak Empire manufacturing survey findings. However, readings are currently forecasted at 51.5 for the manufacturing index and 49.0 for the services index.

The Census Bureau will release their preliminary durable goods orders data for July. Consensus estimates are an expansion of 0.4%, down from 2.0% month-over-month.

International – Japan’s PMI (August 22); Germany’s PMI (August 23); Eurozone’s PMI (August 23); Germany’s ifo survey (August 25)

IHS Markit will release the au Jibun Bank Flash PMI for August. Japanese PMI figures have remained relatively stable between the 50.0-55.0 range for the past 3 months. This pattern is likely to continue because of the strong consumption reported in Japan’s second quarter GDP estimates and supply chains easing.

IHS Markit will release Germany’s August Flash PMI. Germany’s PMI readings turned contractionary in July after high inflation took a toll on input and energy prices. PMI is forecasted to stay contractionary with readings of 48.3 (manufacturing) and 49.0. (services)

IHS Markit will release the eurozone’s Flash PMI for August. During July, the manufacturing PMI turned contractionary as high inflation acted as a headwind on output levels. Consensus estimates are 49.0 for manufacturing and 50.5 for services.

Germany’s ifo will release their business climate survey findings for August. In July, the business climate index fell to 88.6, which was its lowest reading in two years. This was because of a harsh fall in business expectations from rising inflation and Germany’s energy situation. Following this trend, the business climate index is forecasted to continue falling to 86.7.