Weekly Market Pulse - Week ending February 23, 2024

Market developments

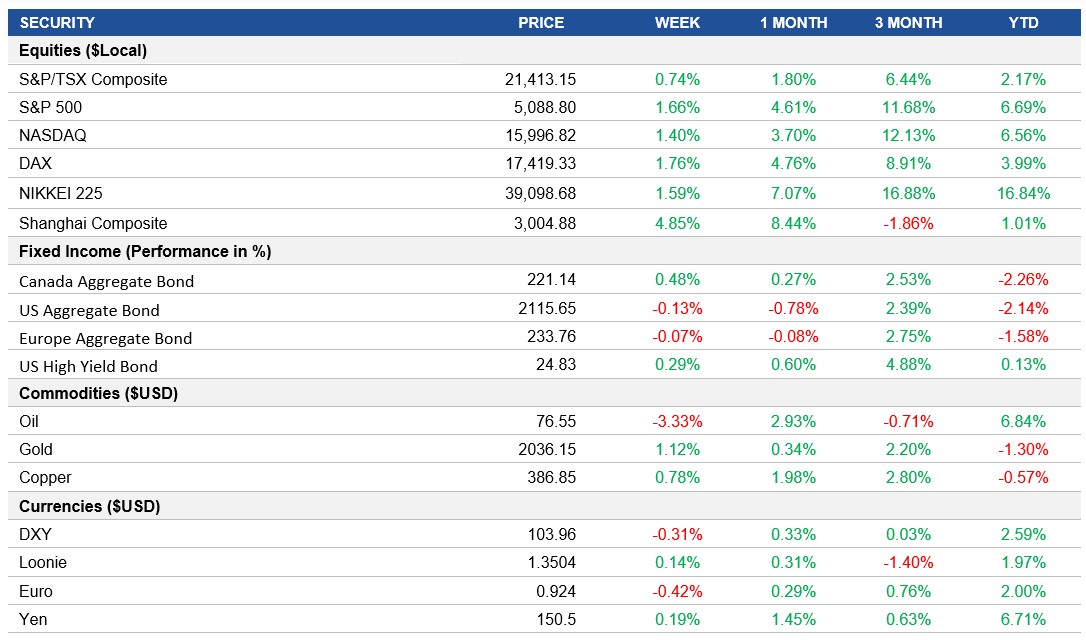

Equities: The equity markets reached new all-time highs this week, with the S&P 500 and NASDAQ indices climbing by 1.66% and 1.40% respectively, marking a continued upward trajectory in investor sentiment and market performance. This positive movement reflects broader market optimism, fueled by robust corporate earnings including the better-than-expected Nvidia Corp.’s earnings report, a key driver in the tech sector. Investors remain keenly focused on corporate earnings to gauge the strength of the market's fundamentals amidst ongoing economic uncertainties.

Fixed income: The fixed income landscape presented a mixed picture this week. The U.S. Aggregate Bond index slightly retreated by 0.13%. This minor pullback reflects the nuanced dynamics within the bond market, driven by evolving expectations around interest rates and inflation. Despite the Federal Reserve's cautious stance on monetary policy adjustments, investors are closely monitoring economic indicators and central bank communications for clues about future rate movements.

Commodities: Crude oil prices experienced a decline due to concerns about extended periods of high interest rates dampening broader economic sentiment, despite signs of a tightening market. West Texas Intermediate futures saw a modest decrease, remaining near the upper bounds of this year's trading range, influenced by geopolitical tensions in the Middle East and strategic output adjustments by OPEC+.

Performance (price return)

Source: Bloomberg, as of February 23, 2024

Macro developments

Canada – Lower Inflation and Slowing Retail Sales

January witnessed a significant cooldown in Canada's inflation, aligning closely with the Bank of Canada's target range. The inflation rate dipped to 2.9%, a figure lower than many had anticipated, signaling a notable variation from previous trends. This decrease was influenced largely by a drop in energy and food prices, marking the smallest rise in these categories for nearly three years. Despite this easing, shelter costs continued their ascent, fueled by rising mortgage interest rates and rental prices, a reflection of Canada's booming population and the cumulative impact of tighter monetary policy on the housing market.

In December, retail sales showed strong growth, supporting an increase in GDP growth with a significant rise in sales volumes. But by January, this growth seemed to slow down, with the preliminary numbers pointing to a likely deceleration in consumer spending and overall economic growth for the first quarter of 2024.

U.S. – Fed Deliberations and Mixed PMI Data

The Federal Reserve's minutes from the late January policy meeting offered insights for both optimistic and cautious market watchers, without explicitly detailing the criteria for gaining "greater confidence" in inflation's return to the 2% target. The discussion highlighted concerns about easing policy too rapidly, emphasizing the need for data-driven decisions on sustainable inflation reduction.

February's PMI flash data pointed to continued economic expansion in the U.S., with the composite output index registering at 51.4, a slight decrease from January's 52.0. This represented a two-month low, signaling a marginal expansion in business activity. The slowdown was particularly noted in the service sector, where the Business Activity Index fell to 51.3 from 52.5, marking a three-month low. Conversely, the Manufacturing PMI improved to 51.5 from January's 50.7, indicating the strongest health of the goods-producing sector in 17 months. These figures highlight a nuanced picture of the U.S. economy, where manufacturing gains contrast with growth challenges in the service sector.

International – Eurozone's Mixed Signals, UK's Resilience, and Japan's Deceleration

In February, the Eurozone saw a slight improvement in its economic downturn, with the Composite PMI Output Index rising to 48.9, marking an eight-month high. The Services PMI reached a stabilizing point at 50.0, suggesting a halt to the sector's decline. However, manufacturing continued to struggle, with both the Manufacturing Output Index and the Manufacturing PMI recording two-month lows at 46.2 and 46.1, respectively.

The UK's economic activity experienced a boost in February, driven by a solid performance in the service sector. The Flash UK PMI Composite Output Index climbed to 53.3, a nine-month high, with the Services PMI remaining unchanged at 54.3. While manufacturing output improved to a three-month high, the sector continues to face contraction. New business volumes across the private sector grew at their fastest pace since May 2023, supported predominantly by service sector gains.

Japan's manufacturing activity dropped to its lowest in over three years, with the au Jibun Bank purchasing managers index for the sector falling to 47.2 in February. This marks a continued period of contraction, as the index has remained below the 50 threshold for nine months. This downturn in manufacturing, alongside an economic recession triggered by weak domestic demand and uncertain external demand, poses a challenge for the Bank of Japan as it considers adjusting its stimulative policy.

Quick look ahead

As of February 23, 2024