Weekly Market Pulse - Week ending July 28, 2023

Market developments

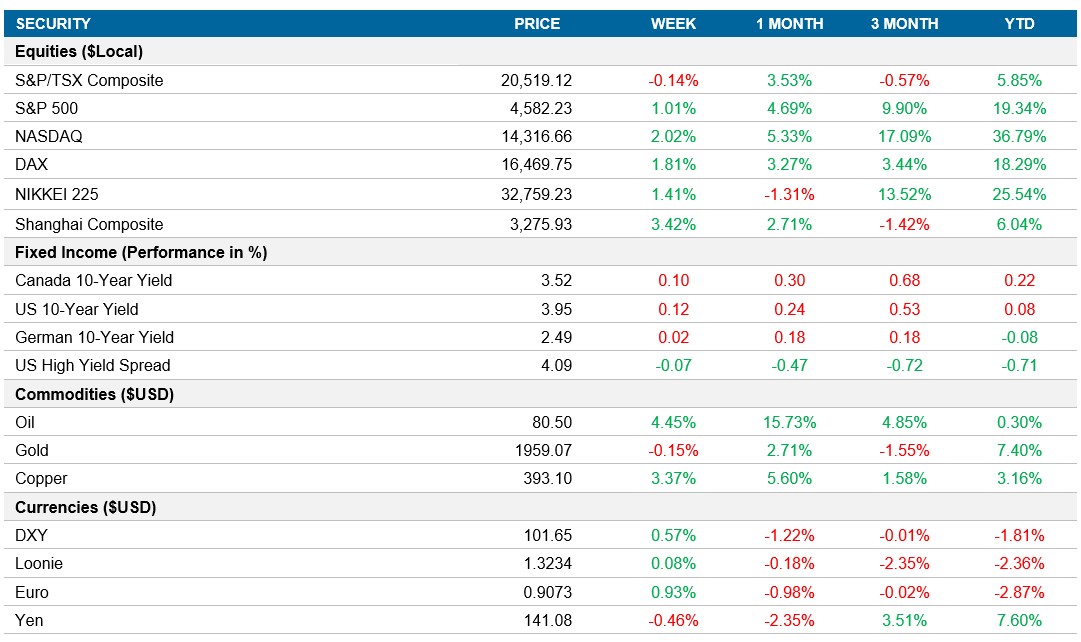

Equities: Investors remain optimistic as U.S. data supports the “Goldilocks” scenario of a balanced economy with key inflation indicators easing while positive economic outlook fuels speculation that the economy can avoid a recession. Tech firms' earnings continued to signal optimism for a soft landing, with AI remaining a focal point. The market has seen a strong rally amid decreasing inflation, steady economy, and better-than-expected Q2 earnings reports in the U.S., the S&P 500 and Nasdaq gaining 1% and 2% respectively.

Fixed income: The Fed remains cautious about ruling out additional rate hikes, with strong data suggesting a prolonged tightening cycle. However, indicators currently point towards a relatively soft landing, and as long as the labor market remains tight and inflation stays above the 2% target, further rate increases are expected in the coming months. Investors appear reassured that tighter monetary policy has not yet pushed the economy towards a recession. U.S. 10yr yields ended the week up 12bps to 3.95%, while the Canadian 10yr rate closed at 3.51%, up 10bps on the week.

Commodities: Oil's weekly gains reached a one-year high, driven by tightening global supplies and expectations of the Federal Reserve's eventual easing of tightening measures. OPEC+ actions, China's stimulus, and improving global demand supported the rally, pushing the price $80 per barrel. However, traders anticipate potential corrections due to overbought conditions and volatility.

Performance (price return)

As of July 28, 2023

Macro developments

Canada – Canadian GDP Rebounded in May, Unlikely to Sustain

Despite a 0.3% m/m rise in GDP in May, the growth in the second quarter is projected to be weaker than expected, with some factors supporting GDP set to unwind. The rebound in May is considered temporary, and June's preliminary estimate suggests a 0.2% m/m contraction, indicating a sharp slowdown in GDP growth. The impact of higher interest rates and fading support from easing supply shortages are expected to further disappoint growth forecasts in the third quarter, according to analysts.

U.S. – Federal Reserve Raises Interest Rates in July, July Sees Slowdown in U.S. Private Sector Activity and PMI Drops to 52.0, U.S. Economy Grows 2.4% in Q2 2023

The Federal Reserve increased the target range for the federal funds rate by 25 basis points to 5.25%-5.5%, in line with market expectations, resulting in the highest borrowing costs since January 2001. Policymakers stated their commitment to monitoring incoming economic information and are prepared to adjust monetary policy as needed to address potential risks to inflation and employment goals. The Fed resumed tightening after the pause in June, citing a moderate pace of economic expansion, robust job gains, low unemployment, and persistent elevated inflation.

U.S. Composite PMI dropped to 52.0 in July, the slowest expansion since February. Service activity growth declined, manufacturing output remained stable, and new orders rose slightly. Job creation was weak, input prices increased moderately, and business confidence hit a year low.

The U.S. economy expanded at an annualized rate of 2.4% in Q2 2023, higher than the previous quarter's 2%, and surpassing market expectations of 1.8%. Non-residential fixed investment accelerated, while consumer spending slowed sharply but still exceeded market estimates.

International – ECB Raises Rates to Tackle Inflation Surge, UK Private Sector Growth Slows in July, Eurozone Composite PMI Records Steepest Contraction in July, Bank of Japan Adopts Flexible Yield Curve Policy, Maintains Rates, Japan Composite PMI Unchanged at 52.1 in July

The ECB raised interest rates by 25 basis points, the ninth consecutive hike, citing persistently high inflation despite a recent slowdown. The main refinancing operations rate now stands at 4.25%, the highest since October 2008, while the deposit facility rate reached 3.75%, the highest in over 22 years. The ECB plans to maintain restrictive rates until inflation returns to its 2% target.

The S&P Global/CIPS United Kingdom Composite PMI fell to 50.7 in July, indicating the weakest growth in the private sector since January. Service sector activity and manufacturing production declined amid rising interest rates, inflation, and economic uncertainty. New business volumes stalled, job creation eased, and price increases were the smallest since February 2021. Business activity expectations also moderated to a seven-month low.

Eurozone Composite PMI fell to 48.9 in July, the steepest contraction since November, with declining new business inflows and backlogs of work. Employment growth slowed, price pressures moderated, and business confidence hit a low since November.

The BoJ kept its key short-term interest rate at -0.1% and maintained the 10-year bond yield around 0% in its July meeting with a unanimous vote. They decided to increase flexibility in its yield curve control policy to enhance the sustainability of stimulus efforts. The board mentioned a moderate economic recovery driven by pent-up demand and expectations of decelerating CPI due to fading effects of past import price rises.

Japan's au Jibun Bank Composite PMI remained steady at 52.1 in July, showing the seventh month of private sector growth but at the slowest rate since February. Services sector expanded for the 11th consecutive month, while manufacturing activity contracted for the sixth time this year. Input price inflation accelerated, and output prices rose faster. However, new orders, employment, and foreign sales experienced softer growth, and backlogs of work declined after previous growth.

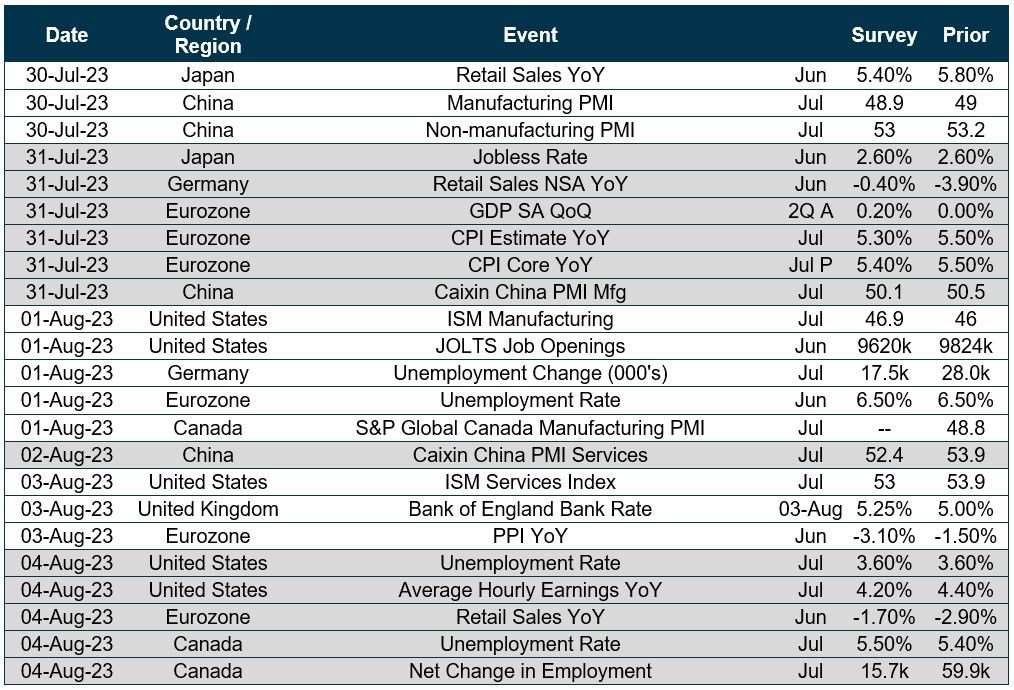

Quick look ahead

As of July 28, 2023