Weekly Market Pulse - Week ending May 24, 2024

Market developments

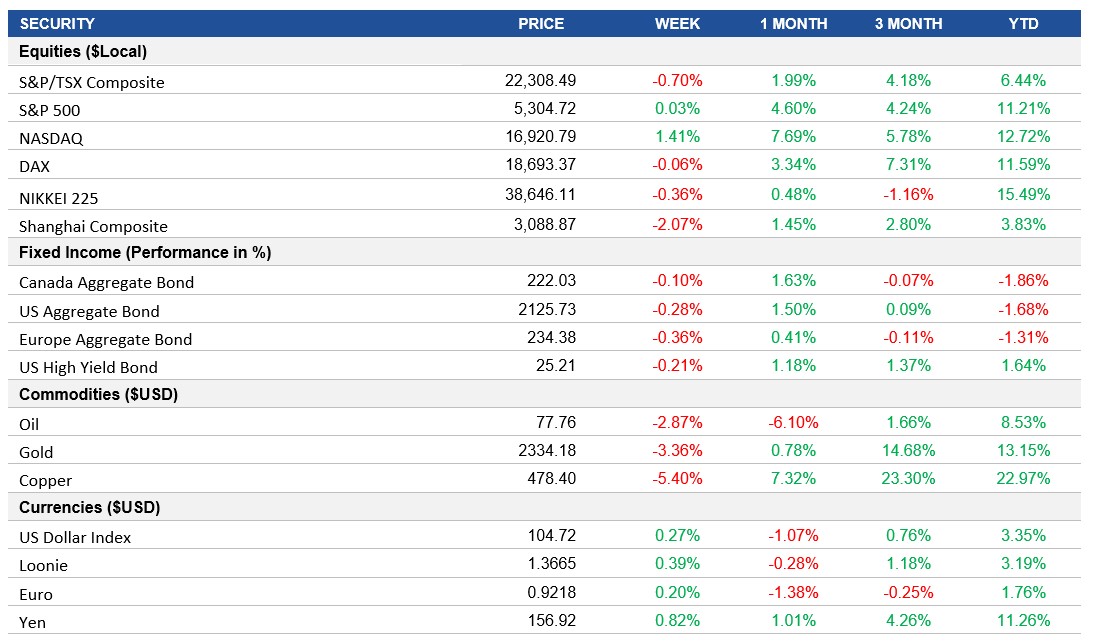

Equities: U.S. stocks climbed after data showed consumers tempered their inflation expectations in late May. The S&P 500 had its fifth straight week of gains, the longest bullish streak since February. It topped 5,300 and the Nasdaq 100 rose 1.7%, with Nvidia heading toward a fresh all-time high after better than expected earnings. However, the equity rally risks overheating according to Bank of America, with 70% of indexes trading above their 50- and 200-day moving averages, nearing a contrarian sell signal.

Fixed Income: While Fed minutes showed openness to further tightening if needed, resilient earnings suggest positive economic news may have less straightforward impact. The tempered inflation expectations bode well for prospects of Fed rate cuts, as easing demand could help bring down inflation. Treasury yields up slightly, with the 2-year yield at 4.93%, as the bond market closed early ahead of the Memorial Day holiday.

Commodities: Oil futures rose on Friday but posted weekly losses as traders feared the Federal Reserve might maintain high interest rates for longer than expected, potentially dampening demand due to an economic slowdown. A lack of clear signals left traders unconvinced, resulting in directionless trading ahead of the U.S. holiday weekend.

Performance (price return)

Source: Bloomberg, as of May 24, 2024

Macro developments

Canada – Canada's Inflation Rate Eases, Canada's Retail Sales Surge

The annual inflation rate in Canada eased to 2.7% in April 2024 from 2.9% in March, marking the slowest rate of consumer price growth since March 2021. This aligns with the Bank of Canada's (BoC) forecast, indicating potential rate cuts. Prices slowed for food and shelter, while transportation costs rose due to higher gasoline prices. The monthly CPI increased by 0.5%.

Retail sales in Canada are projected to have risen by 0.7% in April 2024, the highest in a year, following a 0.2% drop in March. The decline in March was mainly due to a decrease in core retail sales, with significant drops in home furnishings, electronics, and clothing sectors. Gasoline station turnover fell due to higher fuel prices, while motor vehicle sales increased. Annually, retail turnover rose by 1.9%.

U.S. – U.S. Composite PMI Surges

The S&P Global U.S. Composite PMI surged to 54.4 in May, the highest since April 2022, driven by strong growth in the service sector and a positive manufacturing output. Despite job cuts, employment decline slowed, with businesses showing greater confidence. Input costs and output prices rose, with manufacturing leading in price growth, but overall selling price inflation remained below the yearly average.

International – U.K. Composite PMI Declines in May, U.K. Retail Sales Drop, Eurozone Composite PMI Rises to 52.3, Japan Composite PMI Increases, Japan's Inflation Rate Eases

The S&P Global U.K. Composite PMI fell to 52.8 in May, below expectations, yet still indicating solid private sector expansion. Manufacturing production rebounded, but services growth slowed. New orders and export sales increased, though job creation was marginal due to hiring challenges. The rise in selling prices slowed significantly, reflecting reduced input cost inflation.

Retail sales in the U.K. fell by 2.3% month-over-month in April 2024, the largest drop in four months, with declines across most sectors. Non-food store sales, particularly in clothing and furniture, were affected by poor weather and low footfall. Automotive fuel sales also dropped sharply, and food store sales continued their decline. Overall, retail sales fell by 0.7% over the three months to April.

The Eurozone Composite PMI increased to 52.3 in May 2024, the highest in a year, indicating stronger economic recovery. Business activity, new orders, and employment grew, while inflation rates for input costs and output prices softened but remained above pre-pandemic levels. The services sector led the growth, with Germany seeing increased activity and France experiencing a slight output decrease.

The au Jibun Bank Japan Composite PMI rose to 52.4 in May 2024, the highest since last August, indicating continued private sector expansion. The service sector remained strong, and manufacturing output neared stabilization. Employment improved despite slower new orders and a drop in foreign sales. Both input prices and selling charges rose at slower rates, indicating reduced inflation pressures. Sentiment stayed positive despite a slight decline in confidence.

Japan's annual inflation rate decreased to 2.5% in April 2024 from 2.7%, with food prices rising the least in 19 months. Costs eased for furniture, healthcare, and culture, while education prices fell for the first time since May 2021. Transportation costs increased, driven by higher communication prices, and fuel prices dropped the least in 14 months. The core inflation rate dropped to 2.2%, and the monthly CPI rose by 0.2%, the same as in March.

Quick look ahead

As of May 24, 2024