Weekly Market Pulse - Week ending June 28, 2024

Market developments

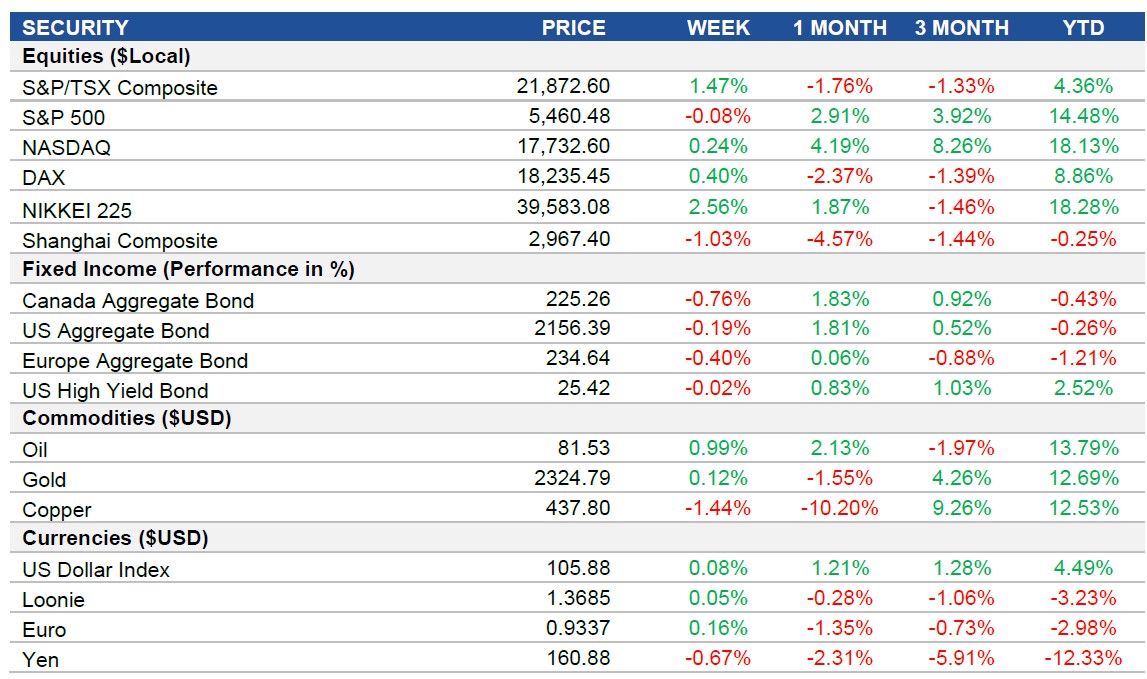

Equities: Stocks rallied towards new all-time highs this week as cooling inflation data strengthened expectations for Federal Reserve interest rate cuts in 2024. The S&P 500 Index touched above 5,500, led by technology stocks, while the Nasdaq approached 18,000. As we hit the halfway mark of the year, the S&P 500 Index has extended its 2024 advance to ~15%, with Nvidia leading gains among megacap stocks.

Fixed Income: The Fed's preferred inflation measure, the PCE price index, showed a deceleration in underlying inflation, boosting investor confidence. Traders now project almost two rate cuts in 2024, with a quarter-point reduction fully priced in by November. However, Federal Reserve officials, including Mary Daly and Thomas Barkin, remain cautious about declaring victory over inflation.

Commodities: Oil only closed slightly higher this week, despite positive economic news and rising geopolitical tensions. The oil market has been generally bullish in June, rebounding from a weak May. This recovery is attributed to improved summer fuel demand outlook and geopolitical tensions, particularly in the Middle East.

Performance (price return)

Source: Bloomberg, as of June 28, 2024

Macro developments

Canada – Rising Inflation in Canada, Economic Growth Outpaces Expectations

The annual inflation rate in Canada increased to 2.9% in May 2024 from 2.7% in April, defying market expectations of a slowdown to 2.6%. This halt in the disinflation trend challenges the anticipation of continued loosening of monetary policy by the Bank of Canada. Prices accelerated in sectors like transportation and food, with notable increases in air transportation and grocery costs, while inflation remained high for shelter and rose in health and personal care.

Canada's GDP rose by 0.3% in April, aligning with preliminary estimates, and a smaller 0.1% rise is expected in May. The growth, driven by sectors like mining and manufacturing, exceeded the Bank of Canada's expectations for the quarter but is unlikely to influence an interest rate cut in July. Despite robust performance, the GDP growth rate is still below the potential growth rate of 2.5%, indicating the economy is not fully utilizing its capacity.

U.S. – U.S. Economic Growth Slows, Stability in U.S. Price Index

The U.S. economy grew at an annualized rate of 1.4% in Q1 2024, slightly above previous estimates but marking the slowest growth since early 2022. Non-residential investment and residential investment saw upward revisions, while consumer spending slowed more than initially anticipated. Government spending and exports increased, while imports decreased, contributing positively to the GDP growth.

The U.S. personal consumption expenditure (PCE) price index was unchanged in May 2024 from April, the least change in six months, following a 0.3% rise in April. Goods prices decreased while services prices increased slightly. The core PCE index rose by 0.1%, the lowest since November. Annual PCE inflation and core PCE inflation both eased to 2.6%, the lowest since March 2021.

International – Stronger-than-Expected U.K. Economic Growth, Japan's Retail Sales Surge

The British economy grew by 0.7% in Q1 2024, higher than initial estimates and marking the strongest expansion in over two years, ending the recession. Growth was driven by the services sector, particularly scientific research and development and legal activities. Household spending increased, driven by recreation, culture, housing, and food. However, gross capital formation and government consumption were lower than expected.

Retail sales in Japan rose by 3% year-on-year in May 2024, surpassing market expectations of 2% growth. This marks the 26th consecutive month of retail sales expansion, fueled by rising wages. Significant sales increases were seen in other retail products, department stores, and machinery & equipment, while sales declined for automobiles and textile, clothing, and personal goods. Monthly retail sales also saw a notable rise.

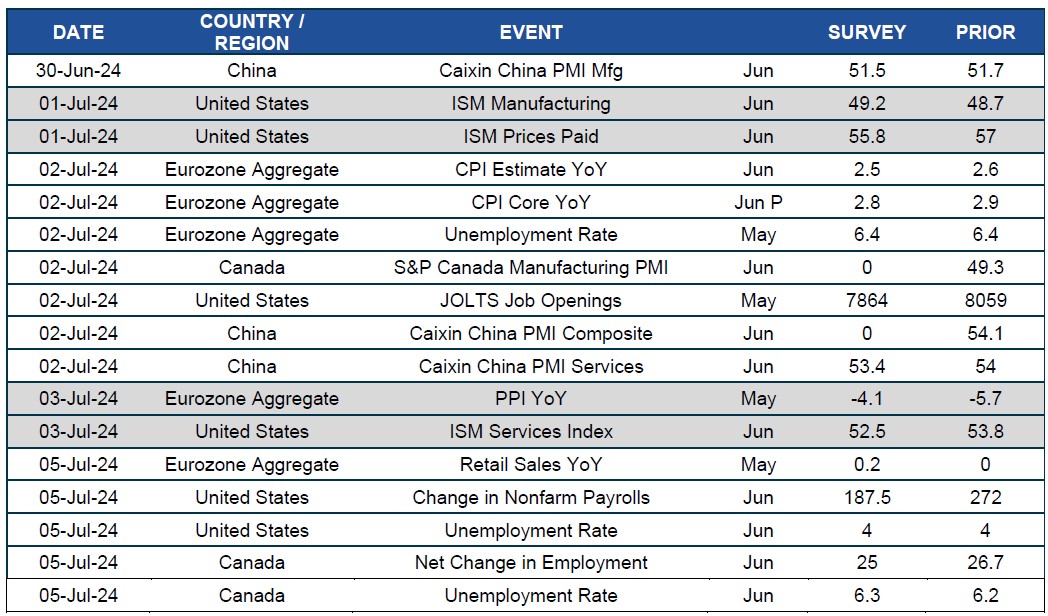

Quick look ahead

As of June 28, 2024