Weekly Market Pulse - Week ending June 23, 2023

Market developments

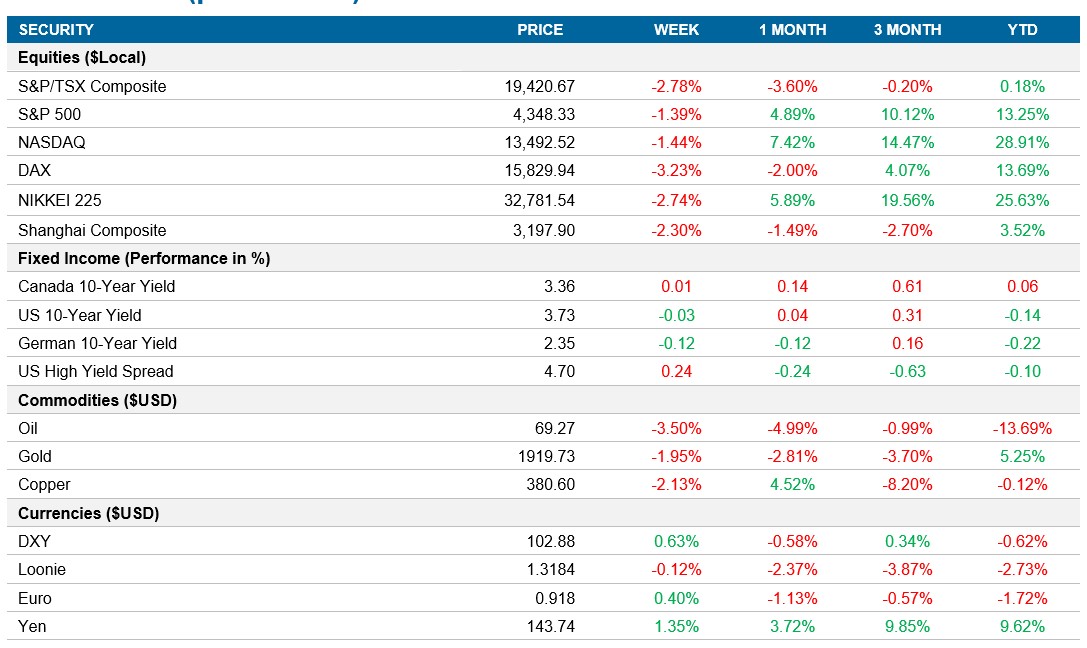

Equities: U.S. stocks retreated, ending the S&P 500's five-week winning streak, as concerns over higher borrowing costs and hawkish signals from central banks resurfaced. The S&P 500 dropped -1.4% for the week with consumer discretionary and information technology sectors performing the worst. With the significant year-to-date gains, there are concerns about stretched valuations and the potential for more rate hikes, as emphasized by Fed Chair Jerome Powell’s remarks on inflation and the possibility of further rate increases in 2023.

Fixed income: Central banks globally are raising rates to control inflation, but there are fears that the Federal Reserve might tighten policy excessively, potentially leading to a recession. Atlanta Fed President Raphael Bostic expressed optimism in defeating inflation without harming the labor market. The Fed recently kept rates unchanged after a series of increases, allowing more time to evaluate the impact of banking stress and higher borrowing costs. The benchmark rate remains in the range of 5% to 5.25% and the U.S. 10yr yields closed ~3.7%

Commodities: Oil prices fell as economic concerns and higher interest rates spooked traders. WTI crude futures dropped 3.5% for the week to $69.25, while Brent crude fell to $73.22. A sluggish global economy, central banks’ focus on inflation, and a strengthening U.S. dollar have contributed to weak oil prices. Traders fear aggressive rate hikes may impact economic growth in the future.

Performance (price return)

As of June 23, 2023

Macro developments

Canada – Canadian Retail Sales Show Resilience with Strong Growth in May

Canadian retail sales are expected to rise by 0.5% in May, following a 1.1% jump in April. Strong sales was seen in general merchandise, food and beverage, specialty food stores, and clothing retailers. Retail volumes grew by 0.3%, indicating consumer resilience. Yearly retail sales advanced by 2.9%.

U.S. – S&P Global U.S. Composite PMI Indicates Slower Private Sector Growth

The S&P Global U.S. Composite PMI dropped to 53.0 in June, signaling a slower upturn in private sector output. Factory production declined sharply, service sector expansion cooled, and job creation slowed. Input cost inflation increased, while selling prices rose at a slower pace.

International – U.K. Consumer Inflation Holds Steady at 8.7% in May, Eurozone Composite PMI Signals Sharp Slowdown in June, Unexpected Decline in Japan’s Annual Inflation Rate to 3.2%

U.K. consumer price inflation remained unchanged at 8.7% in May, staying above the Bank of England's target and raising concerns about its persistence. Rising prices for air travel, recreational goods, and second-hand cars offset falling fuel costs and slower food inflation. The core inflation rate reached 7.1%, the highest in over three decades. The Bank of England responded by rising its policy rate by 50 basis points on June 23rd.

The Eurozone Composite PMI dropped to 50.3 in June, the weakest since January, indicating a significant slowdown in private sector expansion. Manufacturing faced a deepening downturn, while the services sector experienced slower growth. New orders declined, employment growth slowed, and backlogs of work fell sharply. Input costs rose at the slowest rate since December 2020, and average selling prices saw the weakest increase since March 2021. Business optimism for the future also declined due to concerns over demand growth and higher interest rates.

Japan's annual inflation rate declined unexpectedly to 3.2% in May, missing market forecasts of 4.1%. Slower growth in furniture prices and a decrease in fuel and water charges contributed to the decline. However, prices for transport, clothing, medical care, miscellaneous items, and food saw modest increases. Core inflation also dropped to 3.2%, remaining above the Bank of Japan's 2% target for the 14th consecutive month.

Quick look ahead

As of June 23, 2023